- Keep Cool

- Posts

- When the green wave wanes

When the green wave wanes

European parliamentary elections tell a stark story

Nick van Osdol

June 13, 2024

Hey there,

Today we’ll zoom out a bit after a lot of focus on methane recently. Specifically, we’ll cover recent European parliamentary elections. If the specter of the coming U.S. presidential election wasn’t enough for you to think (or not think) about, well, elections elsewhere this year could complicate climate work too.

The newsletter in <50 words: Results from recent European parliamentary elections dealt a blow to green parties across the bloc and call into question where, if anywhere, tailwinds for climate work have the strength to endure. And if political support for climate work can’t endure and isn’t popular, the second-order question is: What’s next?

OPINION

Last week, many countries across the E.U. saw more conservative political groups gain vote share across their parliamentary systems. Here are some results across the biggest countries (by economic size):

Germany: The AfD won 16% of votes, having netted 11% and 13% in 2021 and 2017, and more than Chancellor Olaf Scholz's center-left Social Democrats (14%)

France: Marine Le Pen's National Rally party won more than 30% of the vote, doubling the share President Emmanuel Macron's centrist party won.

Italy: PM Meloni's Fratelli d'Italia won 28% of votes after managing ~6% back in 2019

Needless to say, this isn't great for political support for climate tech and sustainability initiatives. It doesn't necessarily mean existing support for technologies will be rolled back anywhere, but it will make advocating for additional support across the E.U. harder.

Of course, there are countless issues at play in any election. In the wake of the ongoing war between Russia and Ukraine, energy security is indubitably on Europeans' minds. But adequate defense against a belligerent Russia, inflation, immigration, the economy in general, and other issues seem substantially higher in mind than climate and sustainability.

While these topics all converge, and while politicians do recognize that at times – as evidenced by a recent G7 proposal to support clean energy development in Africa to reduce the amount of migrants attempting to immigrate from Northern Africa into Europe via Italy – it doesn't seem like leading on climate or 'green' initiatives has consistently made politicians more popular. Green parties across Europe garnered far fewer votes and parliamentary seats in these elections than they did in 2019. That setback comes in the wake of significant farmer protests in countries like Germany, France, and the Netherlands that pushed back on policies designed to push agricultural systems and economies toward sustainability, and as economically critical industrial sectors in places like Germany struggle to decarbonize.

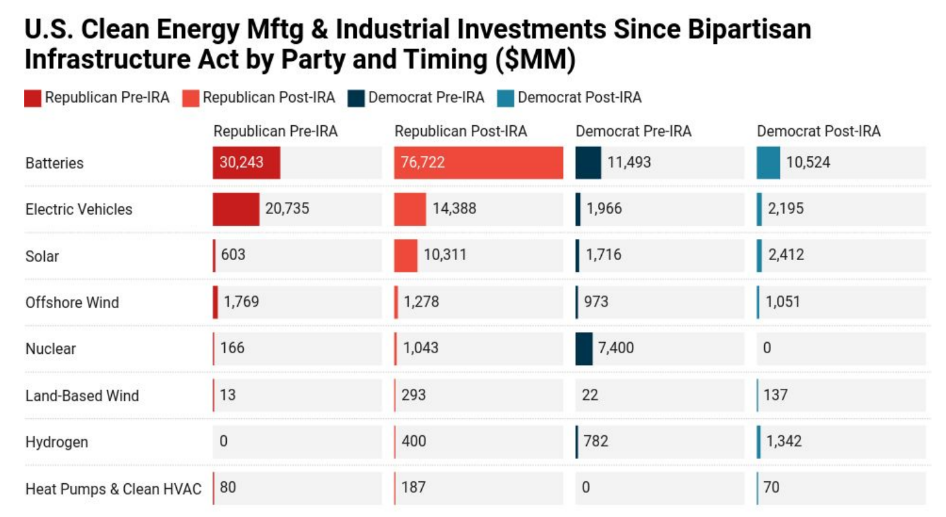

Similarly, while his overall climate record can be checkered by statistics like the fact that U.S. oil and gas production are at all-time highs, Biden has been a much more climate-focused President than most previous. Yet, his approval is lower today than it has been at any point in his presidency. Again, that likely has a lot more to do with people's perception of his age, inflation, economic performance, etc.… Still, considering how much Biden has done to spur climate tech investment in the U.S. (see below), the extent to which that hasn't worked to his credit is striking.

All this raises a key question for me: Has anyone sold sustainability well? Said differently, has anyone figured out how to sell sustainability in a 'sustainable' fashion? Given we're riding a market cycle that has seen considerable renewed enthusiasm, support, and capital for climate technologies and energy transition work, it's important to remember that those tailwinds aren't guaranteed forever.

Selling sustainability poorly

Trying to ‘score’ policy and political parties that are broadly supportive of the energy transition and more sustainable technologies and systems is even more complicated. The questions we’re skirting around aren’t inherently about whether it’s worth it to undertake an energy transition, support more sustainable agriculture, decarbonize industry, or rebuild domestic manufacturing bases. Nor are they inherently about whether the policy that’s been put into place is working or not. Often, as with Biden’s IRA policies in red states, there’s little he could offer that would sway many people’s minds.

Rather, registering the political landscape halfway through 2024 and 4-5 years into a climate tech 2.0 boom, it’s worth asking whether the narratives upon which the current boom depends are running out of steam. The capital-raising environment for startups has already shifted; it was easier for climate tech companies to raise money last year than it is today, and several venture-backed climate companies go out of business weekly now.

Now, we’re seeing political support shift, too. Even if existing policy support for climate tech in Europe isn’t rolled back, the fact that it will now be much harder to provide additional or new policy support likely represents a change to many people and organizations’ forward-looking projections. Whether consciously or subconsciously, I think many of us have assumed for the past few years that the policy environment in Europe, especially, would become more and more supportive over time. We can’t assume that anymore.

Taking on the question of why the political sphere has shifted is one that plunges us much more into psychology than discussions about technology, innovation, or price. Though perhaps there’s still overlap, especially in storytelling. For instance, for years, the story that renewable energy is cheaper than fossil fuels has been quite strong, and it’s been sold to consumers in both Europe and the U.S., where, in many places, renewable energy penetration has grown remarkably. Still, in many, if not most, of these places, the prices that customers pay are stubbornly high, if not at all-time highs.

In California, for instance, a state that’s an undisputed leader in solar and also battery deployment, electricity rates are skyrocketing. There’s plenty of technical and regulatory decomposition needed to understand why; for instance, transmission and distribution costs make up a much larger share of what U.S. customers now pay for electricity than they once did. Still, it isn’t impossible to divine the experience of the layperson here. Even the more immediate supposed benefits of climate technologies, on which they’ve often been sold and heavily subsidized, haven’t come to bear. That’s a bad experience to foist on voters, and perhaps we’re starting to reap what we sowed.

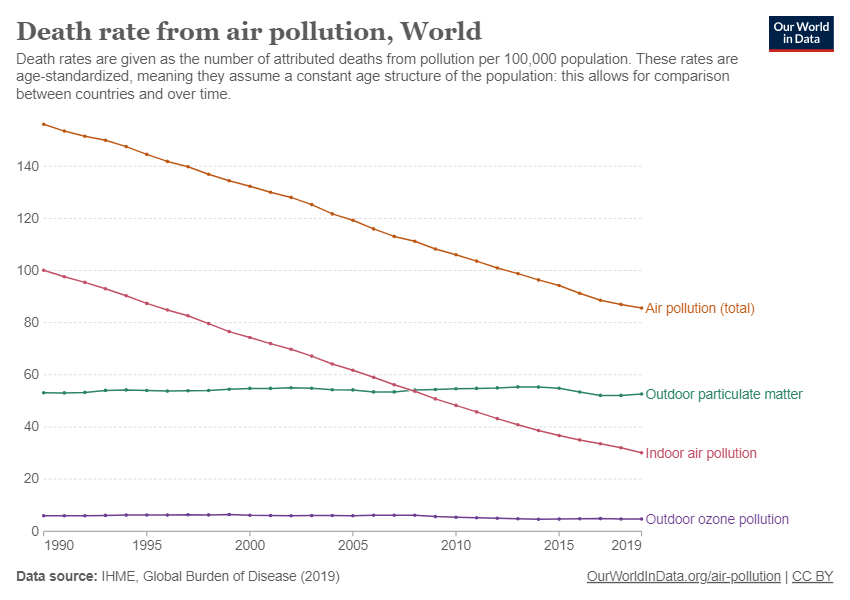

Meanwhile, the benefits of things like reduced air pollution of renewable energy or EVs are probably drastically under-sold. Since the 90s, annual deaths attributable to air pollution in the U.S. have nearly halved. No small part of that decrease likely stems from the closure of coal power plants, tighter tailpipe emissions regulations, and more tech and policy trends that all count as ‘climate.’

Similar trends also hold globally. Perhaps we should be selling those types of stats instead, as they contribute to an optimistic story that’s real and here.

What Europe exports to the world

While Europe exports a lot less material stuff to the rest of the world than it once did, it still played an important leadership role in climate policy, innovation, and deployment so far this century. Hence, the problem with Europe and the U.S. potentially abnegating pole position in terms of their climate and energy transition leadership has less, ultimately, to do with Europe and the U.S. or their emissions and broader ecological impact. Increasingly, any and all climate conversations need to focus on how to cajole and convince countries like India and China, together home to more than a third of the world’s people and 40% of global greenhouse gas emissions, to follow global leadership on energy transition and climate work from elsewhere.

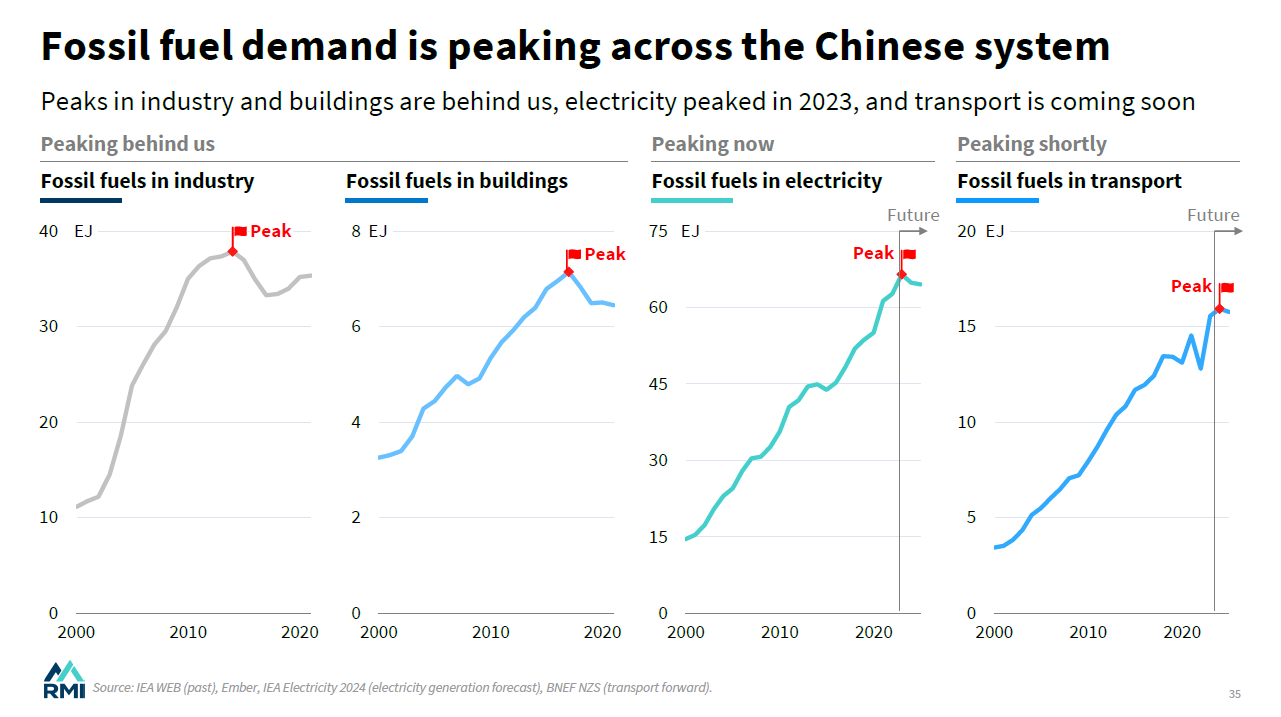

We’ve discussed how important the Chinese, Indian, and other Asian power sectors are to global decarbonization previously. While some recent reports and models suggest Chinese emissions may have peaked, peaking is a far cry from emissions falling substantially. China and India together still consume about two-thirds of the world’s coal, and, unlike other geographies globally, their coal demand hasn’t been falling in recent years.

We’ve also previously discussed how important it is that the U.S. and E.U. lead and demonstrate the viability of decarbonization solutions across sectors, because, well, it’s not always clear who else is going to. China does deploy a lot of renewable energy and nuclear power, indeed, perhaps China has done the best job of any country at making climate tech part and parcel of economic growth. Still, if you look at other sectors, such as steel manufacturing, Chinese companies lag the decarbonization efforts of their U.S. peers considerably.

The same can be said about agriculture. India has more cows than anywhere else in the world, and the majority are owned by smallholder farmers whose cattle you can count on one hand. India is the world’s largest dairy-producing country (also has 1.4B people), producing something like a third of the world’s milk. Those cows also produce a lot of methane emissions. Similarly, China is a major reason that demand for meat is growing globally rather than waning.

All of this reinforces another question: What happens if the U.S. and the E.U. lead on climate efforts less? Many countries that are coming up the income curve, including but not limited to India and China, will feel they have the option to ease off or slow their climate efforts, too.

The net-net

Saying “we” need to do X, Y, and Z to slow global warming or achieve other ecological goals has always been imprecise. Who is this ‘we’? All humans? That’s convenient, but indigenous tribes in the Amazon have had nothing to do with tipping Earth’s climate systems out of balance. Is it fair to lump them into a universal group and allot them responsibility for reversing scenarios they had no hand in creating and, in fact, have done more than most to ameliorate?

When we get more precise with our ‘we’s,’ perhaps ‘we’d’ find ourselves zeroing in on sufficiently resourced constituents of countries that have historically manufactured a lot of the greenhouse gasses already in the atmosphere and created and benefitted from prevailing global economic systems. Troublingly, if ‘we’ went through that ‘we’-defining exercise, we’d likely identify a set of stakeholders that are in the process of leaning away from climate work and the energy transition again, at least politically.

What’s at risk is that the loose, royal, amorphous ‘we’ that ‘we’ often use to capture the essence of people and organizations that care about climate technologies, policy, and innovation globally is getting smaller, not larger. That’s a more significant risk to climate efforts than probably anything else right now. At least until the U.S. votes in November, it’ll remain so.

KEEP COOL PODCAST

Here’s the latest on the podcast front: Tom Ferguson, Founder and Managing Partner at Burnt Island Ventures, and I discuss what the hell it even means to “invest in water.” Tom’s perspective on this matter is unique, as his is one of the first venture capital firms focused on doing just that, namely investing in startups driving innovation in water-focused applications and industries.

Like many other topics we cover here, ranging from methane to geoengineering and more, despite touching nearly everything on Earth, water is an under-discussed, under-invested in, and under-resourced category. As a result, innovation in the space often lags other areas that get more attention, whether fintech, crypto, or AI. At the same time, water is one of several categories that could see the most disruption due to climate change. Hence, (and suffice it to say) Tom & I had plenty to discuss in this conversation. Check it out here.

Have a nice weekend ahead,

— Nick

Reply