- Keep Cool

- Posts

- Spooky season

Hi,

Halloween is approaching, which means it's ~spooky~ season. Simultaneously, things are getting a bit ~spooky~ for some if not much of the climate tech ecosystem. Let’s talk about it.

H/t to my bestie Mark Grace, who helped make this piece a lot better.

The newsletter in 50 words: Climate tech ‘vibes’ are entering a spooky season. What’s to be done? First, zoom out to appreciate how business cycles will impact climate and energy tech businesses as long as we exist in the confines of a capitalist market system. Second, grieve as needed. Then, keep on keeping on.

OPINION

If I were to keep a longer ‘crypt list’ of climate tech companies that have gone under of late, these would feature promintently (just from 3 months and change):

Sunpower, an integrated solar manufacturer and installer that went public in 2005 and was once valued at more than $1B, announced bankruptcy in August.

Lumio, a U.S.-based residential solar company that had previously raised hundreds of millions, filed for bankruptcy earlier this month.

Motif FoodWorks, which originally spun out of Ginkgo Bioworks and raised $345 million since 2019, including a monster $226 million Series B, shuttered last month.

Swell Energy, a U.S. business that wanted to aggregate distributed energy in residential settings to build VPPs, shut down in August. The company had raised hundreds of millions.

Universal Hydrogen, which was developing hydrogen-powered aircraft and had raised $85 million, also closed its doors at the end of last quarter.

The list goes on, especially if you extend it to companies that are struggling but haven’t yet folded. For instance, earlier this week, reporting from Sifted highlighted that Lilium, an eVTOL developer that raised $114 million in equity funding in May, is showing signs of financial distress. Similarly, Ynsect, which has raised more than $600 million, also filed a safeguard plan as it’s running short on cash.

Together, the first five businesses called out above represent billions of investor capital. In the grand scheme of things, that isn’t that much money. Still, if you’re a venture capitalist or a watcher of their doings, we’re in a ‘back-to-reality’ moment after a frothy start to the decade.

Even at the latest stage of the venture-backed company lifecycle, there are signs of trouble. Northvolt, the Swedish battery manufacturing darling (though perhaps investors and customers aren’t as sweet on it as they once were), was supposed to close to an IPO, which would have been a welcome signpost of success in otherwise choppy seas for (and a welcome liquidity event for investors) the industry. Now, the company is reducing its workforce by 20%, selling a factory in Sweden and Poland, and announcing that its largest factory is also delayed, all after BMW canceled a $2 billion contract.

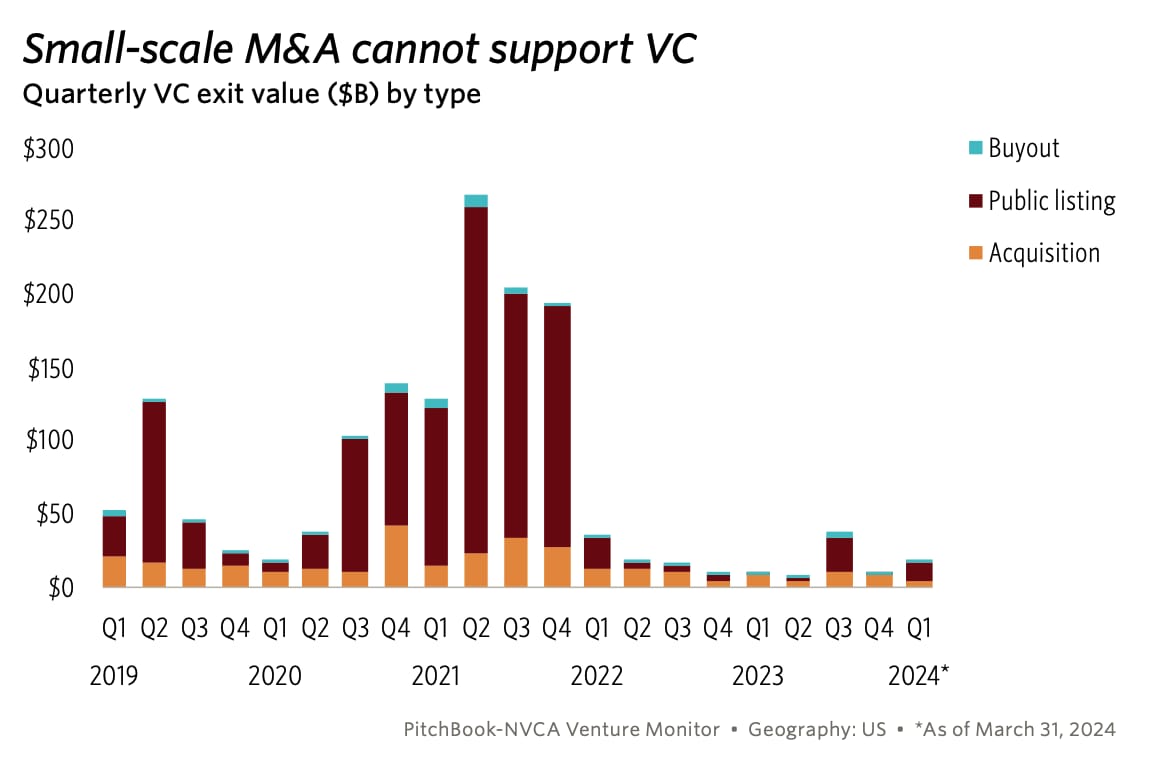

In addition to businesses shutting down, there is also less M&A now than in late 2020 and 2021, which impacts whether and when investors (and operators) see returns:

Let it suffice that both a slowdown in investing from the early 2020s is now well documented and palplable and that this has been true for long enough that companies that were charting a longer path to profitability—and were thus reliant on iteratively securing new funding—are running into trouble.

As a result, it feels like some, if not many, of us are in a bit of a ‘sad girl mode.’ Friends are having a hard time fundraising. Friends are getting laid off. Friends are having a hard time finding new work. You get the idea.

Sad girl mode is welcome—dare I say needed—sometimes. I’m in it often. It’s a healthy response; many folks are stretched thin, frenetically trying to hit milestones, trying to make the proverbial reaper wait a quarter or two. This may sound strange, but it’s good to have periods where we admit to ourselves that everything isn’t gravy. Trying to restitch the foundations of the modern economy in a more sustainable fashion was and is never going to be an easy task. And sometimes, it is time to fold on one idea, clear space, re-set, and prepare for the next endeavor or adventure. So take this season of really feeling the feelings. Take your time. But don’t get disenfranchised or give up entirely (if you can).

Keep cool, people.

I don’t want to downplay the significance of what’s going on to those who lost jobs and worked hard to develop and commercialize new technologies and services at the companies listed above, as well as many others that have gone under. It is simultaneously true that all of this—whether ‘this’ refers to investment slowdowns, businesses shutting down, or the general ‘vibes’ not being what they were two years ago—is part of the stochastic market cycle. Unfortunately, climate-focused businesses are no more immune to this reality, per se, than pizza shops. As I wrote a few months ago:

Whether we’re discussing a venture-backed business that raised more than $50M in capital or a laundromat on your block financed with a mix of bank loans and someone’s personal savings, the modal assumption about the long-term business outcome should be the same: The business will die.

Over the years, many people have told me their businesses will succeed because the world needs what they’re doing for climate reasons. Unfortunately, what the world needs and what the market wants are often not the same thing, which is one reason why so many pernicious, system-level issues continue to plague the world in the first place, including climate change-related challenges but also many others, whether war, healthcare, or something else entirely.

Further, venture capital is not some foundational bulwark of the energy transition or climate change mitigation and adaptation. It is a very relevant and needed component of the capital stack. I work in it myself. But it’s a small one compared to public funding from governments or debt / project financing.

Finally, whether in nature itself or in private markets, destruction is an integral part of innovation. That idea, of creative destruction, owes back to Joseph Schumpeter, who wrote:

...in capitalist reality as distinguished from its textbook picture, [what matters is]… the competition from the new commodity, the new technology, the new source of supply, the new type of organization (the largest-scale unit of control for instance)—competition which commands a decisive cost or quality advantage and which strikes not at the margins of the profits and the outputs of the existing firms but at their foundations and their very lives.

In the words of poet William Carlos Williams, we’re seeing “the rare occurrence of the expected.” Challenging times, especially in the wake of jubilent times, are to be expected.

Seeing the circle in the cycle

A fundamental misalignment between business and nature upon which I often reflect is that cycles of death (which really just means transformation) are second 'nature' to nature but aren't privileged or promoted as a ‘normal,’ let alone healthy in business, markets, and technology. In business and technology, we like lines that go up and to the right, ideally exponentially. We try to hit milestones on quarterly and annual cycles, where each cycle elevates the lofty goals of the preceding one. Nature, meanwhile, moves in cycles that are inherently much more circular. Spring brings rebirth while Winter heralds in a 'dying,' but it's a 'dying' that sets the precondition for rebirth. Of the spring.

If it’s a more circular, sustainability economy we want, there’s a lot to learn from the extent to which nature, without fail, embraces that pattern as a deeply engrained modus operandi. As climate tech undergoes a 'digestion' phase, i.e., one in which things aren't as fun, exciting, or well-funded as they were, say, two years ago, we should:

See it as a precondition for the next spring rather than an end entirely

Ask better questions about where to go from here

Ask ourselves which innovative technologies or novel approaches are real 'incumbent-killers' and 'paradigm-shifters.'

It's perilously easy to swing from one pole to another, to shout the ascendance of climate tech from the rooftops in 2021 only to masochistically announce its death knell in 2024. Sure, Donald Trump could come in like a wrecking ball and destroy foundational pillars of financial support in the U.S. in a few short months. The global warming reality we’re living in feels increasingly grim. Still, this doesn’t mean we should cling too dearly to self-pity, casting blame around elsewhere, or feelings of apathy. Nor should we ardently espouse overly simple explanations for failure, such as that “the fossil fuel lobby is too strong.”

Technologies like solar, EVs, batteries, and more aren't going away, even if subsidy support subsides. Deployment could slow—definitely. But there are and will be many more 'unkillable' innovations from this century that help make climate progress, even if the extent to which they can entirely 'kill' fossil fuels remains unclear. I don't pretend to know precisely which of the many technologies they are. But they're out there.

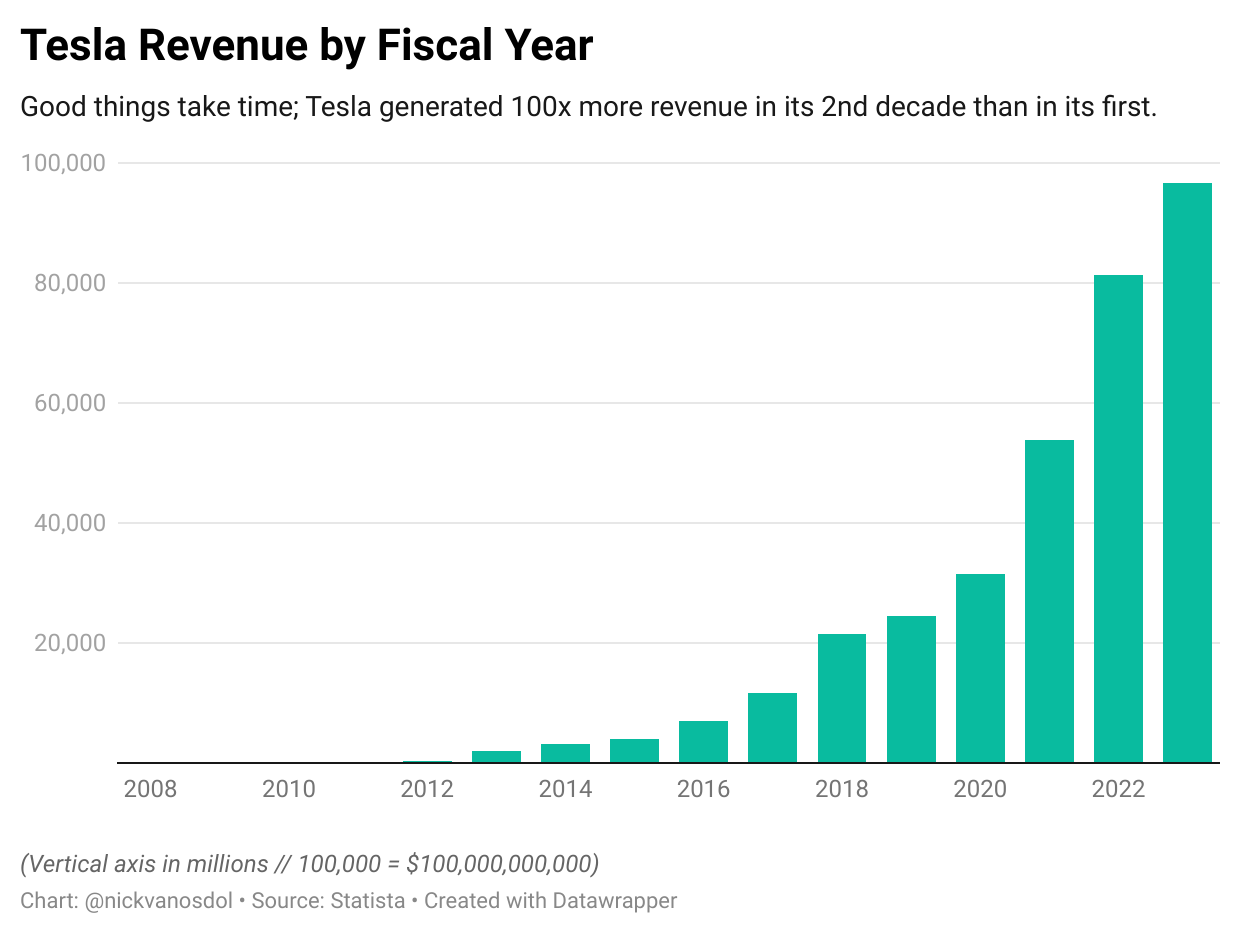

Tesla, founded in 2003 and now worth hundreds of billions, is a crystallization of the fact that EVs are, at minimum, a threat to kill combustion engines and that there was / is good business in building on top of that innovation. Tesla's revenue in 2013 was roughly $2 billion. In 2023, it was almost $100 billion (publicly available info in 10-Ks).

Much of the climate tech ecosystem, in its current incarnation, isn’t there yet. There have been few to zero relevant IPOs from companies started over the past decade and most of the climate and energy-adjacent SPACs were money pits for public market investors. However, as Tesla has demonstrated, these things take time. We’re ‘only’ 5-6 years into the ‘climate tech 2.0’ cycle. Tesla almost went under multiple times in its first 5-10 years.

The net-net

Said succintly, I’m not that pessimistic about the business prospects inherent to mitigating climate change and adapting to it. There’s a lot of noise in market cycles. But the cycles are to be expected. Nor will they wipe the entire slate clean. I know plenty of ‘climate tech’ businesses that are thriving and even approaching the vaulted EBITDA positive milestone. The next few years might be rough riding for many, but the companies that survive will form the foundation of the next “good times.” That’s always been how it goes.

Finally, knowing that the ‘frothy start’ to the decade I referenced earlier brought lots of people (myself included) into the climate tech fold for the first time, what’s important is that the absence of ‘froth’ not turn us all off. Let’s not be fair-weather fans, especially as extreme weather intensifies.

Ciao,

— Nick

Reply