- Keep Cool

- Posts

- Is this thing on?

Is this thing on?

On whether the data center story is really that important

Nick van Osdol

December 05, 2024

KEEPING COOL WITH

Hi there,

It’s end-of-year roundup time now that we’re firmly in December (*shudders visibly at my perceived experience of an accelerating passage of time*).

This piece is on the data center demand growth story, a story that has cornered a lot of media airtime this year. To be sure, I think there are other, more important stories across the world of climate change, energy, and other mitigation and adaptation solutions. That said, sometimes you need to step into the story that’s hogging the headlines to parse why it seems so salient to so many. Or, better yet, to determine how to broaden where that attention gets paid and reallocate some of it to its highest and best uses.

The newsletter in 50 words: Data center demand growth is the talk of the town. How ‘real’ is the story? Will exponential demand growth strain grids and doom companies’ sustainability goals? Even more importantly, how can we take the stranglehold this story has on people’s attention and broaden the scope of what we focus on?

PRESENTED BY SUPERCRITICAL

If you need to get up to speed on what's up in the world of nature-based solutions, Supercritical's latest report is for you. From the basics of credible community agroforestry to case studies, it's a deep dive into trends and insights that can boost your expertise, business, and climate outcomes in 2025.

Download it here.

DEEP DIVE

One of the biggest stories in 2024 in energy circles was indubitably the forecast growth in electricity needs driven by heightened demand for data centers. The increased desire for data centers follows on the heels of the massive wave of interest in and demand for AI, machine learning, and the slurry of other words that describe a whole host of computing-intensive applications.

Wait. Pause. Should this be one of the biggest stories of 2024? I’ll poke and prod at that question a bit in here. Said differently: Is this thing actually on?

The data dump

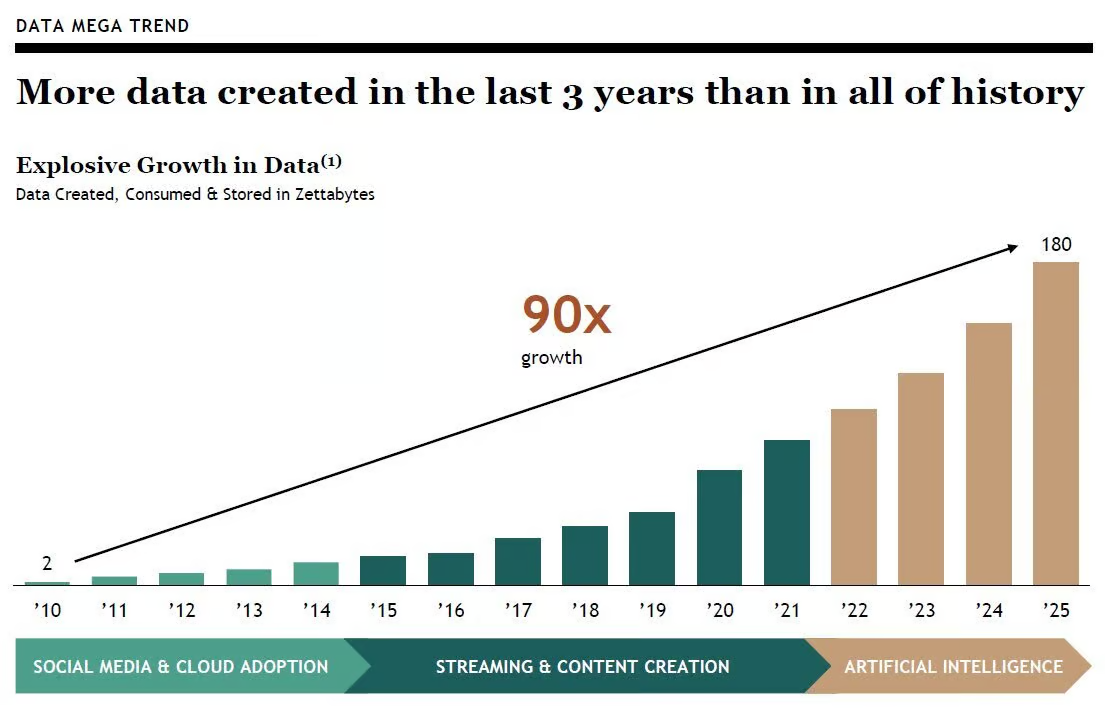

It is ‘indubitably’ true that the amount of data the world produces and makes efforts to store, manage, and process is growing exponentially. A statistic that has stuck with me since first encountering it is that China used more concrete between 2011 and 2013 than the U.S. did in the 20th century. Similarly, the world produced more data in the past three years than in all human history preceding it, whether you measure data in books in libraries or photos taken on iPhones 1 through 13.

Against this backdrop, forecasts for data center demand are skyrocketing. I doubt I need to parrot off too many headlines here; you’ve likely seen many, and a few more will suffice:

$1T+ spent building data centers over the next few years on data centers and the infrastructure to power them (Goldman Sachs)

1.7T / year gallons of freshwater demand from data centers by 2027 (Deloitte).

800+ TWh/yr by U.S. data centers by 2026 (IEA).

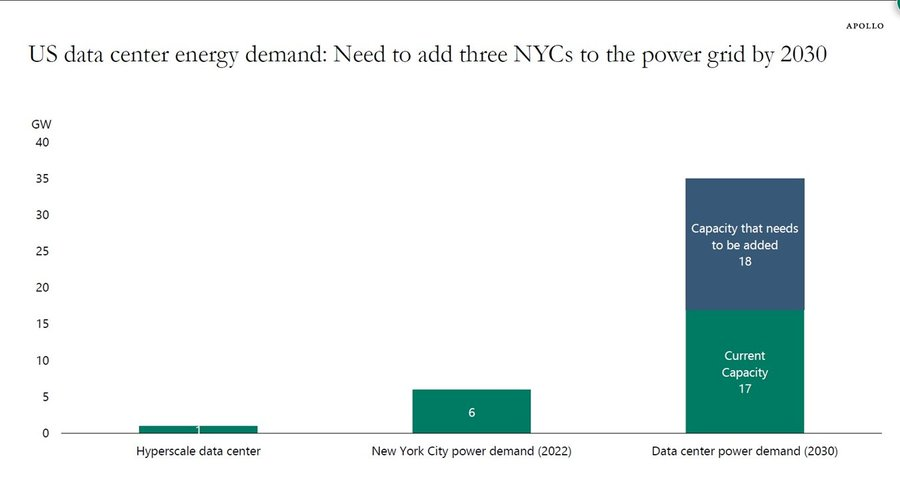

Additional data center power demand forecasts in the U.S. out to say, 2030, could represent the addition of electricity demand equivalent to 3 NYCs (Apollo).

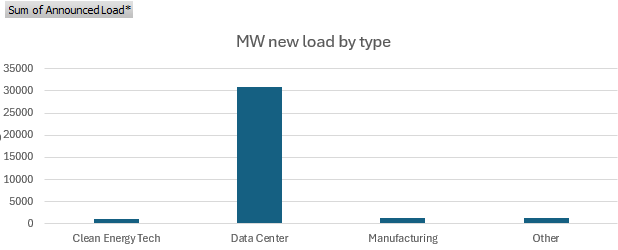

Analyzing utilities’ plans tells a similar story. Georgia Power’s (the largest subsidiary of Southern Company, one of the U.S.’s largest electricity generators) recent load growth forecast is basically all data center-driven demand. (h/t to Simon Mahan for this one):

These latest ‘load growth’ projections from Georgia Power ballooned by roughly 50% to 36.5 MW since its last round of projections, primarily due to the forecast data center demand visualized above. Its 2028 to 2029 pipeline, in particular, tripled from 6 GW to nearly 20 GW. To put this in perspective, the two most recent nuclear reactors completed in Georgia offer about 2 GW of capacity (and were way over budget and delivered far later than original target dates).

In light of this, staggering partnerships and investment announcements are coming to the fore. For instance, last month, KKR and Energy Capital Partners announced a $50 billion “strategic partnership” to invest in new data centers and to otherwise support growth in computing for AI. Similarly, BlackRock, Global Infrastructure Partners, Microsoft, and MGX—an AI investor—announced a $100 billion partnership to invest in data centers and support power infrastructure in September, too.

All of this is exciting at one level; while AI may well be overhyped in some cases, it can and will indubitably do many cool things for humanity. Advances enabled by more computing power will unlock “wins” across many applications, as has been true for decades already. For instance, advances in DNA sequencing (with significant cost reductions) are a success story that depended in large part on advances in computing over the past decades. In the future, other health-related progress (as one focal example) may well be wonderful. For a recent example, as noted in VentureBeat:

“Google DeepMind has unexpectedly released the source code and model weights of AlphaFold 3 for academic use, marking a significant advance that could accelerate scientific discovery and drug development. The surprise announcement comes just weeks after the system’s creators, Demis Hassabis and John Jumper, were awarded the 2024 Nobel Prize in Chemistry for their work on protein structure prediction.”

But all this work does hinge on more data center capacity, which raises costs and challenges:

Cost: Building a data center costs $10+ million per MW of power capacity (Morgan Stanley) just for construction. A GW facility thus requires a $10+ billion investment before purchasing the computers, accounting for cooling needs, etc.... (Note: power production is a fraction of total build costs, though power availability matters a lot).

Power: Power capacity is a primary constraint in building new data centers. Real estate with high-power infrastructure and power availability is exceptionally high in demand.

Semiconductors (‘chips’): There’s massive demand for semiconductors (such as those made by NVIDIA, currently the world’s most valuable company) that power computers. Hence, there are also intense backlogs for additional chips.

Still, returning to the Chinese concrete statistic from earlier, that continues to strike me as more remarkable than forecasts for data center construction demand growth and whatever else it may require.

For one, the advent of cloud computing, increased internet speed and internet access globally, and more sophisticated, powerful computers, whether in data centers or our pockets, is a trend that’s been percolating for some time—its acceleration doesn’t surprise me that much. Many massive businesses are already built on top of collecting your data, whether to target advertisements at you more precisely or to make remote-operated drones for warfare more, well, “precise.”

Secondly, the concrete stat deals more ‘concretely’ in the physical world, where constraints ranging from power and raw input materials to space for factory development are typically more limited. Physical constraints are germane to data centers, too, but as we’ll get into shortly, there’s a lot more advancement in technological efficiencies in the data center world than in the cement-making world.

Thirdly, concrete production is a much more greenhouse gas emissions-intensive enterprise than all of the world’s computing needs (by a factor of more than 10).

Of course, that last point could change. Through some combination of advanced cement and concrete production that shifts the process from an emissions-intensive one to a less emissions-intensive one, or by way of a massive surge in how much power is used by data centers and computers, there’s an imaginable future in which computing overtakes concrete as a bigger greenhouse gas emissions and hence, climate change, story.

I do not think that specific version of the future is ours, though.

A data center in Noord Holland, The Netherlands (Shutterstock)

Case studies in efficiency

Here’s the meat: why am I not that obsessed with this story, at least as typically presented?

For one, data center growth has already been a welcome boon for cleaner energy development for many years. Amazon has procured 77 TWh of renewable energy generation so far for its cloud computing and AI needs. Many other players continue to invest in renewables to add cleaner power capacity and mitigate emissions. See here, here, here, and here for recent announcements.

Most importantly, there are big-time efficiency opportunities when it comes to computing, whether in large-scale chip production itself or in the computing capacity of chips themselves. On the former front, chip manufacturers, motivated by eye-watering demand for their products, are well-positioned to invest in improvements in physical production efficiency (see, for instance, Taiwan Semi Conductor’s recent production yield results at a plant in Arizona.)

On the latter front, this entire ‘story’ has been enabled by improvements in computer chips. Decades ago, computers were the size of rooms. Today, chips are dazzlingly dense and tiny.

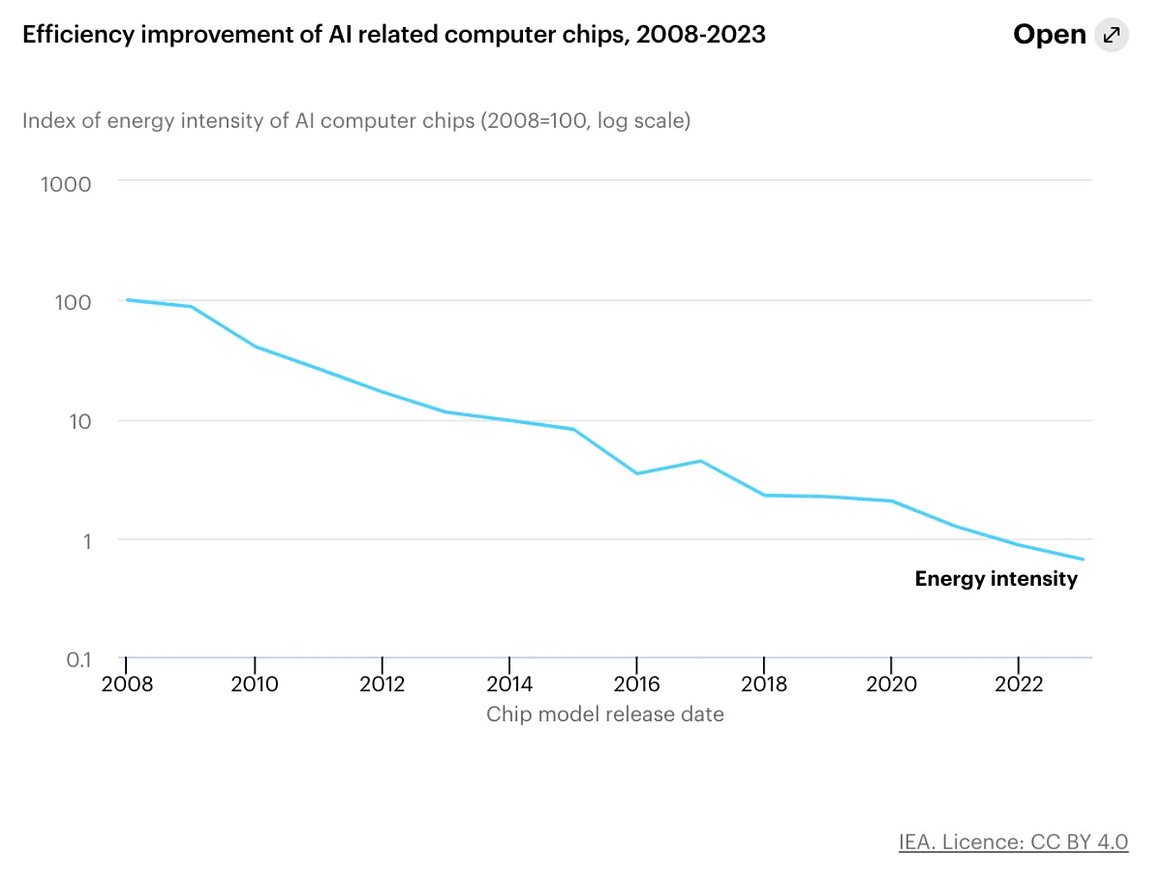

The trend towards increasingly more mind-bogglingly powerful chips in small form factors will continue and could offset rising power demand projections significantly. Efficiency improvements in chips over the past fifteen years are already well documented and support the possibility of further 100x efficiency improvements. As charted by Hannah Ritchie:

NVIDIA’s hottest and highly sought-after new chips, Blackwell-architecture GPUs, could offer up to 96% energy reductions. To date, Nvidia has shipped ~13,000 Blackwell samples to customers and aims to sell billions of dollars worth in financial quarters to come.

If projected chip efficiencies come to bear (even if they’re in the right ballpark), that alone will dramatically cut into forecasts for load growth. Plus, the efficiency conversation also extends well beyond power needs and computing capacity. Today, traditional air cooling can consume up to 50% of electricity in data centers; novel cooling technologies offer significant opportunities to reduce cost, power demands, emissions, and more.

To recap so far, my take here is that efficiency gains across the data center hardware and software stack may temper the higher end of data center demand growth forecasts considerably. The corollary I’ll draw is every past red flag that’s been raised about copper, lithium, or oil shortfalls. What invariably happens when demand for a commodity materializes is that we find new ways to accommodate it. The world has never run out of a commodity; when demand spikes, new supply usually ‘magically’ materializes (it’s not magic; it’s markets).

Caveats for the computers

All the above said, it is tautologically true that the data center demand growth story is ‘real.’ Demand is going up. Plus, as long as a story runs laps around the right people’s minds (as this story is currently doing, ranging from utility CEOs to tech executives and, clearly, even my own), then the story is very real insofar as it hogs our own built-in computers’ (our brains’) available capacity.

Further, beyond the scope of the construction, investment, and additional power consumption needed for data centers, there are other reasons the story is compelling. Data centers could become ideal test beds for first-of-a-kind (‘FOAK’) projects for new energy generation, distribution, and storage technologies and projects. This is already happening and is a big positive: Fervo Energy already has an operational FOAK project for its advanced geothermal energy technologies and approaches in Nevada that it is expanding to service Google’s increasing low-emission power needs.

Similarly, data center demand forecasts have offered a boon to the nuclear energy industry, of late, which has otherwise languished in the U.S. for decades. Announcements like the following have been a dime a dozen over the past few months:

Data centers could also become a catalyst for environmental and permitting reform, which may be a bright spot for the new, otherwise climate-disoriented U.S. federal administration. Insofar as tech companies' plans to develop novel energy infrastructure to power data centers are or would at times get thwarted by environmental restrictions (see a recent Meta-backed plan for a nuclear-powered data center that was sunk by a rare bee species), it stands to reason companies will throw their lobbying weight behind reforms that could make building cleaner energy infrastructure easier.

Finally, data centers could also drive closer collaboration between utilities and other stakeholders who intersect and need to collaborate, at least to a degree, when facing increased power needs. Most data centers are grid-connected assets; few are built on a proverbial “island.” That’s unlikely to change soon. While somewhat flexible in their power usage, data centers require, at minimum, reasonably consistent power access, which is not something ‘transient’ renewables like wind and solar alone, or even solar and wind paired with battery energy storage systems, can accommodate. As noted by David Porter of the Electric Power Research Institute recently (quoted in Axios here):

"Porter also said hyperscalers and utilities can better collaborate on timing of data center construction and arrival of new power assets."

All that’s welcome!

Caveats on the caveats

…That said, there’s also a real risk a short-term shortfall in data center capacity could yield additional, long-lived fossil fuel-focused infrastructure. For instance, Dominion Energy, a large U.S. utility, released plans earlier this year to add 21 GW of clean energy by 2039. It also penciled in almost 6 GW of new gas generation simultaneously. If and when operational, it’s hard to see Dominion deprecating that new gas capacity earlier than needed when you consider the investments needed to develop it. Similarly, Entergy, another major U.S. utility, recently proposed 1.5 GW of new natural gas generation capacity to power a data center in Louisiana.

Further, as welcome as the revival of retired nuclear power plants or even new (potentially small, modular, advanced nuclear power plants) would be, long lead times for nuclear development risk serving as a smokescreen for companies who commit to reviving, building, and/or paying for power from them. Consider this hypothetical:

If I’m a tech company and I want to shore up my promises to push for a more sustainable way of doing business, and I need more data centers, saying I will pay to develop an advanced nuclear power plant on my site does a few things.

My announcement and intentions may be based in truth. I (the tech company) may be 100% serious about working with the developer to build the plant, complete with needed approvals.

The deal may signal to my investors, customers, and regulators that I’m still committed to reducing emissions and other environmental impacts from my operations.

But the deal may also allow me to continue business as usual, sourcing electricity from a grid connection, with power serviced by a utility (that may be building more gas plants to meet demand), at least as long as everyone waits for the nuclear plant to get built or certified for resumed operation.

The problem here is that nuclear development plans often take longer than expected (even if the expectations are already decadal). Or they may not come to fruition at all, especially as far as new reactor designs are concerned.

In this hypothetical, neither the tech company, the developer, nor the utility has necessarily done anything wrong. However, the tech company has effectively mortgaged all the emissions that persisted throughout the proposed nuclear plant development phase for a reduction in future emissions. If the plans then fail through or take longer than anticipated, the future emissions reductions remain unrealized or, at minimum, the actual emissions reduction is lower than initially imagined.

In the worst-case scenario, where the plant development is abandoned, the tech company and its developer have failed to build the proverbial ‘house,’ leaving everyone with no salve for future emissions and a backlog of emissions from the development phase that could have been abated otherwise, such as with solar, wind, and batteries, to offset some of the emissions from the start.

Opening our aperture

When we zoom out globally and even in the U.S., data center demand, no matter how robust the forecast you choose, will remain a small portion of the overall drivers of electricity demand growth. China has expanded its electricity production more than fourfold over the past decade or so. Little to none of this has anything to do with data centers.

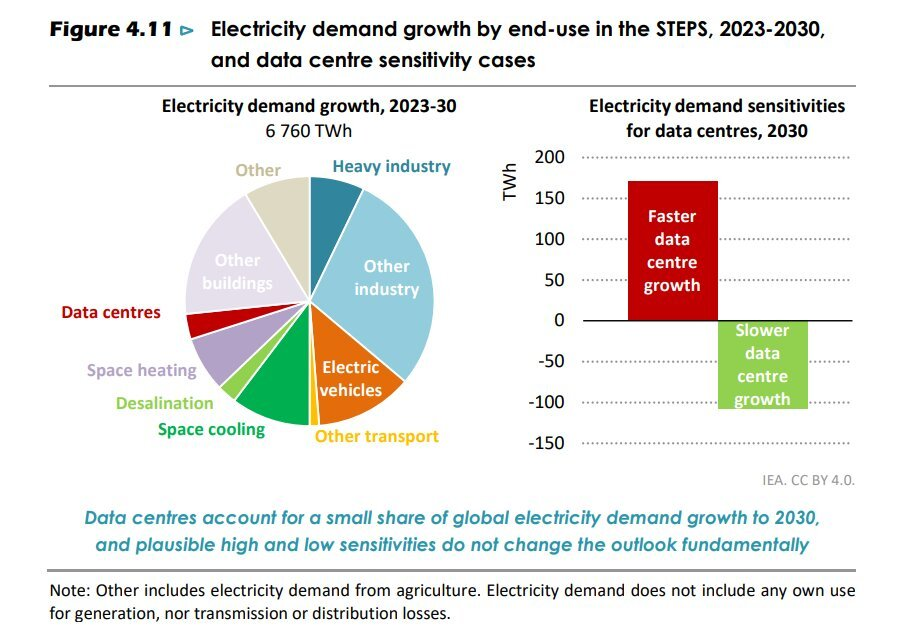

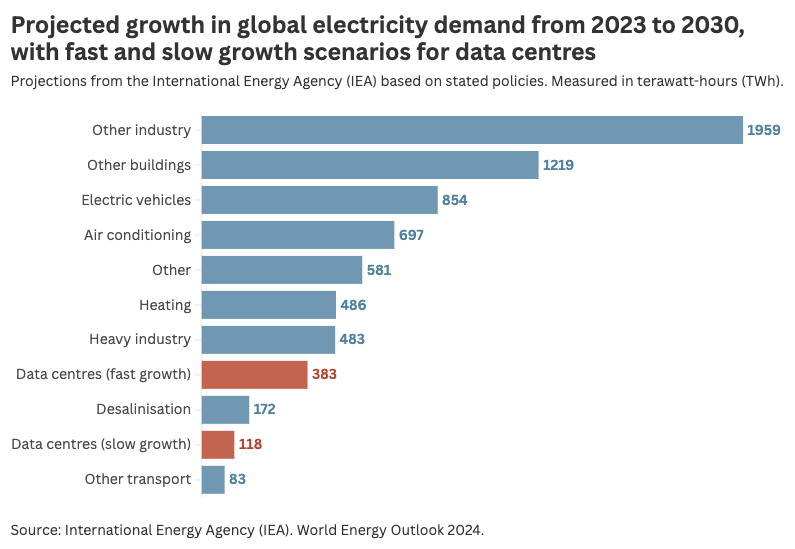

Globally, if we analyze projected electricity demand growth out to 2030, as the IEA did in its annual World Energy Outlook report (2024 version referenced), data centers comprise only a small sliver of the total electricity demand growth pie. I ate much larger slices of pumpkin pie last week, probably ones more commensurate with “Other industry.”

To put a finer point on this thought expansion exercise, as examined and illustrated (in the following chart after the quote) by Hannah Ritchie in a recent topical piece (linked 7 words ago):

“These projections are very uncertain. The IEA tried to put bounds on the sensitivity of these estimates by publishing ‘fast AI growth’ and ‘slow AI growth’ scenarios. In the chart below I’ve shown where these would rank. Even in the fast growth scenario, data centres don’t move up the list of the big drivers of electricity demand.”

Suffice it to say, the data center story may be a bit myopic, the same way climate and energy-focused communications often are (mine included). As long as we’re going to spend time discussing things, it’s helpful to ‘open the aperture’ to bring other ideas into the fold.

The net-net

The data center story is ultimately a perfectly relevant and interesting one, as it’s an intersection point between countless macro trends across energy and climate, whether demand growth versus efficiency gains or the tension between innovation, the rising electricity demands invariably innovation adds, and the urgent need for decarbonization.

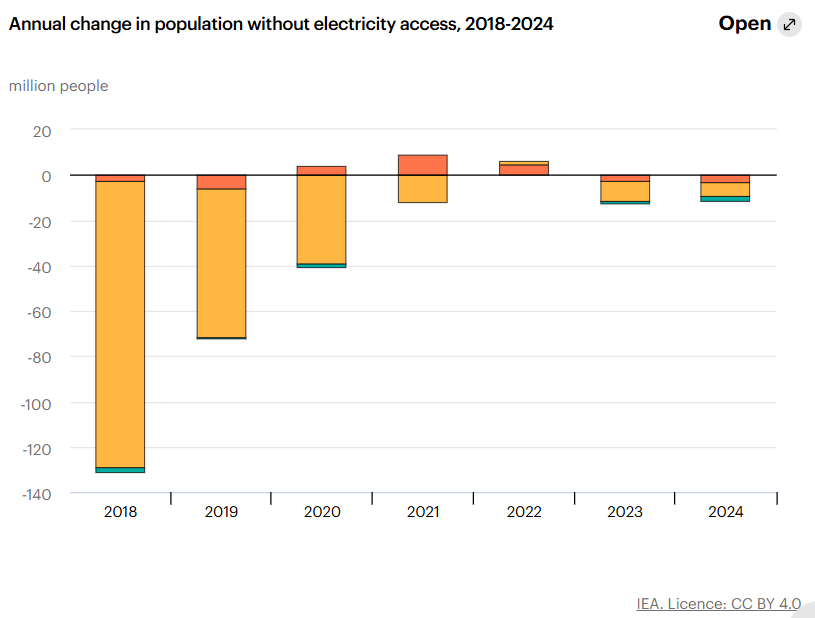

But if we choose to harp on data center demand growth, we might as well discuss load growth across countless needs and technologies. In some places, the need is far more fundamental to survival than what AI applications enabled by more computing can offer. In many countries, the average citizen’s access to air conditioning (life-saving), electricity in general (significantly life-improving), and even things most of us take for granted, like clothes washing (also dramatically life-improving).

I’d like to see gains in electricity access (above) expand more rapidly (source: IEA)

Ultimately, we can use the data center discussion to refine our thinking and, ideally, drive change around how we create and allocate more power, raw materials, or capital across all its forms—from dollars to human labor hours and our attention. In my mind, that’s the highest and best takeaway from this story. The demand growth ‘hockey-stick’ will happen again. How we handle it now will inevitably inform how we handle it in the future.

For a more esoteric note to close on in the vein of how we allocate our attention (which is about as close an equivalent to data center capacity as you’ll get in human form), I’ll quote from my favorite book I read this year, “The Unforgiveable” by Cristina Campo:

“To ask a man to never be distracted, to be continually turning his faculty of attention away from the errors of imagination, the laziness of habit, the hypnosis of custom, is to ask him to realize his highest form… It is to ask him for something very close to holiness in a time that seems to be pursuing, with blind fury and bone-chilling success, nothing so much as a total divorce of the human mind from its capacity for attention.”

Have a nice rest of your week, and see you here again Sunday,

— Nick

Reply