- Keep Cool

- Posts

- How not to control the narrative

How not to control the narrative

Nick van Osdol

November 05, 2023

We’ve previously discussed challenges in wind energy, particularly offshore.

I do this because it’s my job to try to stay as balanced and clear-sighted as possible with respect to the climate tech and energy landscape. While it’s also important that I add to a sense of optimism and buoy folks’ belief in the energy transition and decarbonization, I’m not here to be a dogmatic champion of any one technology or set of technologies.

Especially when a technology or tech category is faltering.

Unfortunately, this week added to the increasingly stark picture for wind energy. Ørsted formally scrapped two U.S. offshore wind projects and recorded an additional $4B impairment on top of previous billion-dollar impairments. Mind you, that’s a $4B impairment for a company that had a ~$20B market cap.

Get bent: Major players in wind power are having a bit of a breakdown (Shutterstock)

Earlier this year, Avangrid paid a total of $64M to terminate U.S. offshore wind power purchase agreements to “avoid billions of dollars in write-offs,” stating the projects, in general, were “unfinanceable.” I’d consider all offshore wind projects in the U.S., even those that are outwardly moving forward, as ‘at risk’.

But things aren’t just bleak for offshore wind in the U.S. In Germany, Siemens Energy, one of the largest wind turbine manufacturers, is seeking up to $15B in guarantees from the German government amidst mounting problems with its wind turbine manufacturing division.

Similarly, GE, which also makes turbines, offered investors advanced guidance that their wind division will post billion dollar losses in 2023 & 2024. GM took $2.2B in losses from its renewable energy division in 2022, too. Clearly, their path to manufacturing profitability remains much further out than expected.

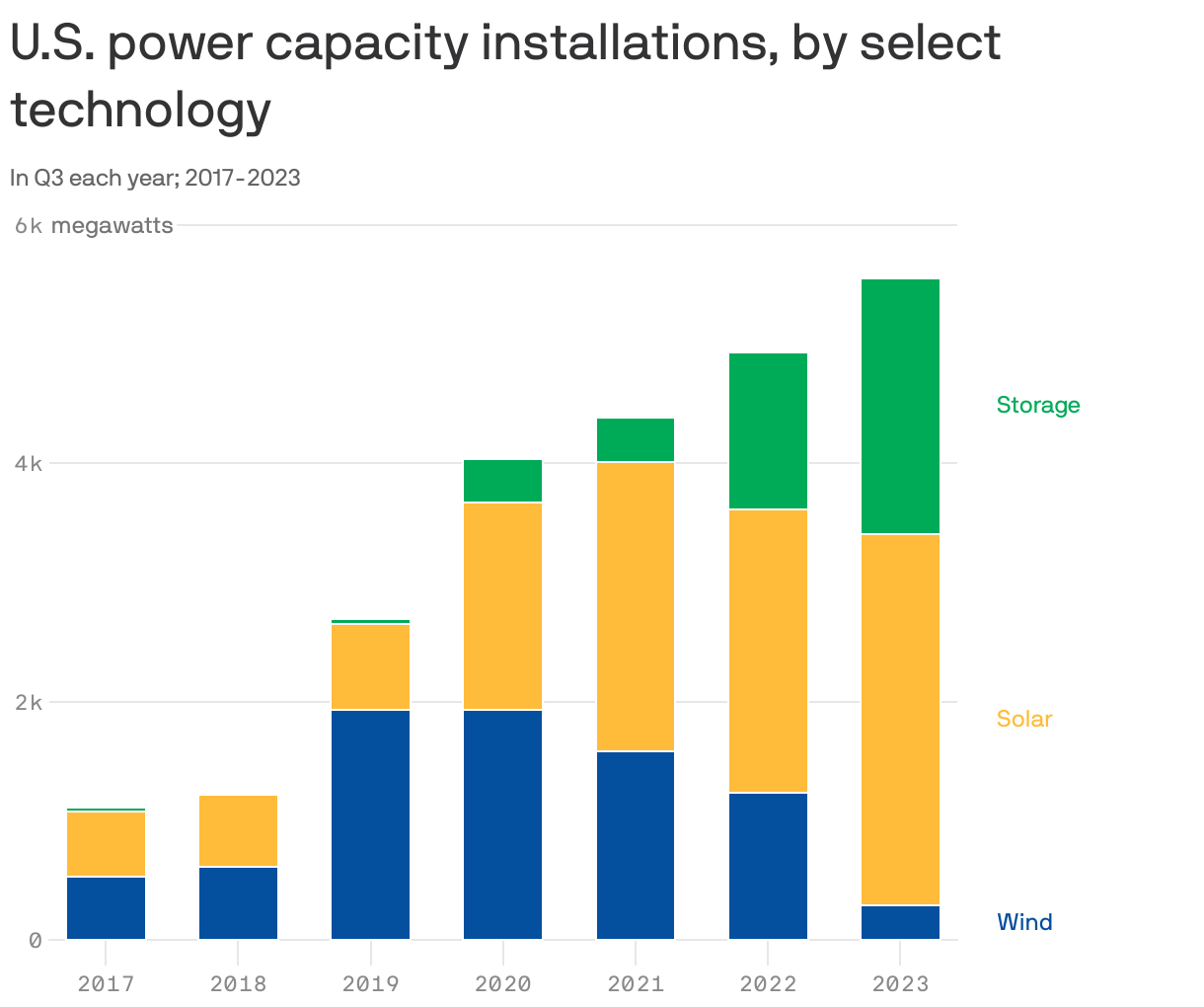

This all goes beyond manufacturing, too. In terms of deployment, things have slowed to a crawl for wind in the U.S. The below graphic from Axios illustrates just how little wind energy capacity has been deployed this year.

Data: American Clean Power Association; Chart: Axios Visuals

Some of this slowdown has to do with well-documented interconnection backlogs. But if solar and storage are still getting through the queue (in record numbers), you have to ask yourself, why is no one finishing wind projects?

In terms of causes, it’s worth clarifying at least two things are happening concurrently here:

Offshore wind projects are getting canceled, and, as per the above chart, onshore projects aren’t being deployed, or at least finalized, readily either.

Manufacturers like Siemens Energy and GE are finding it very difficult to make and sell wind turbines.

The second challenge is perhaps more concerning than the first. Project cancellations may have more to do with ‘supply chain issues’ and higher interest rates (both of which I’ve spoken to in recent newsletters and linked above).

But more fundamentally, if non-Chinese turbine manufacturers can’t make money, that is a threatening and structural challenge. As I cited from a recent Siemens Gamesa financial disclosure, some of the mounting difficulties for turbine manufacturers stem from higher-than-anticipated maintenance costs:

The impact of the outcome of the periodic monitoring and technical failure assessment of the installed fleet amounted to c. -€472m in EBIT pre-PPA and before integration and restructuring costs. The assessment, which detected a negative trend in specific component failure rates, resulted in higher projected maintenance and warranty expenses than had been estimated previously.

Said more simply, turbines are breaking down more quickly than expected, across a variety of environments and installed projects. Not good!

How not to control the narrative

Narratives are as crucial to the success of the energy transition as anything else. If I didn’t believe that, I wouldn’t be spending time writing this newsletter twice a week.

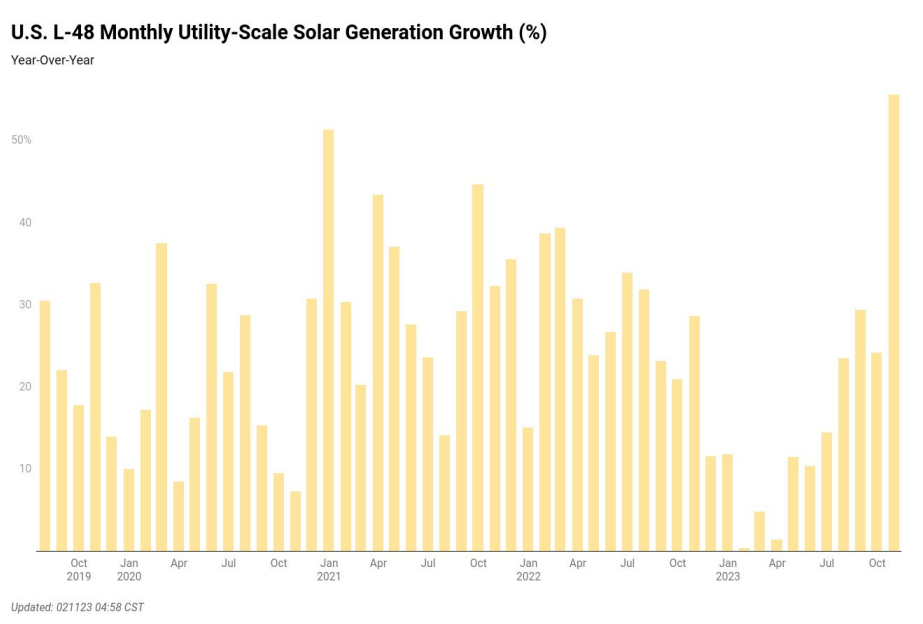

The problem with what’s happening in wind isn’t necessarily at the level of existing operating assets. Many renewable energy assets worldwide are doing fine, generating electricity, making their owners money, making grids more reliable, and helping keep utility bills down for consumers.

To illustrate the fact that many renewable energy assets, especially solar, are doing fine, see below for monthly year-over-year generation growth in the U.S. Mind you, these aren’t capacity additions; the chart illustrates growth in generation (also worth noting October 2023 was abnormally sunny).

Chart courtesy of enersection (see here)

Suffice it to say that solar is fine.

Perhaps wind as a category will be back on track soon, too, maybe as early as 2025, and the challenges we’re hitting on here will be behind us. I sure hope so.

The problem is that everything happening in wind right now means we – i.e., the folks who want to see a speedy, efficient, ethical clean energy transition – could and probably already are losing control of the narrative.

Media headlines are one thing. They matter. But there are other touchpoints for citizens, consumers, and voters that are souring as the wind falters.

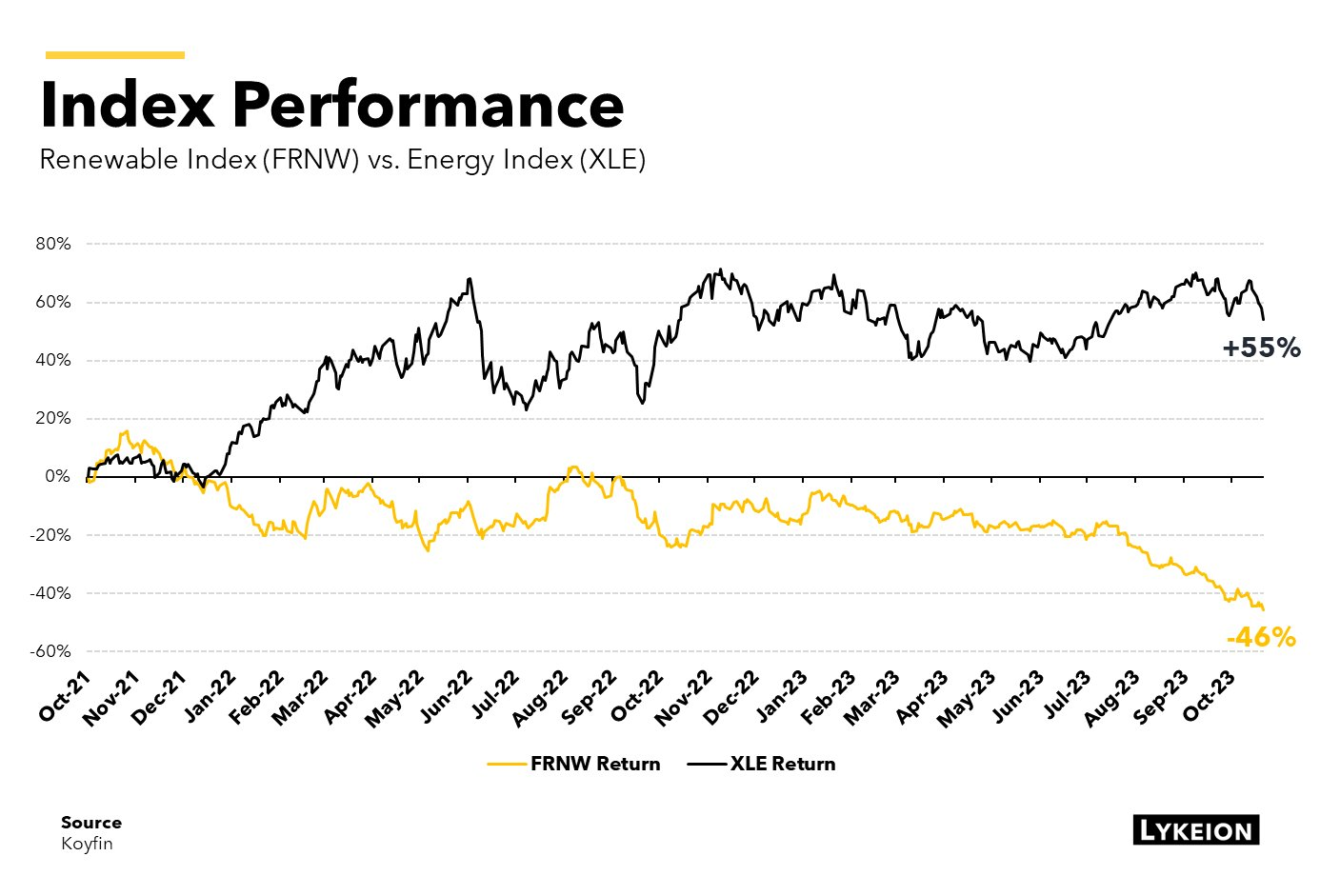

For instance, the primary avenue for everyday investors to get exposure to the energy transition and renewables is by investing in the equity of OEMs, utilities, or project developers and operators. All these public equities and ETFs have offered dramatically negative returns for the past ~2 years, especially over the past few weeks. And they’re performing worse than the oil and gas companies.

This is a real problem, almost a crisis in my opinion, as far as the confidence of the layperson in the energy transition and renewable energy is concerned. To reiterate, it is perhaps more of a problem of narrative and appearances. But that doesn’t make it any less ‘real’ than, say, a hardware problem.

If folks were sold on the narrative of renewable energy being the de facto best and most efficient energy source in the world and shifted some of their money into renewable energy companies over the past years accordingly, they’ve now lost a lot of that money. If I had done that, I’d be a) mad and b) would be questioning the bullish narratives about renewables I was sold on.

Stated differently, challenges in wind energy project financing, deployment, and manufacturing threaten to derail the entire renewable energy sector’s mojo. How should a hypothetical New Jersey resident feel when Ørsted backs out of two offshore wind projects in their state – projects that, mind you, were previously loudly championed – stating they’re suddenly too expensive? Mind you, many of these people, through no fault of their own, barely know there are tax credits available to them to buy EVs. Put yourself in their shoes. What conclusion would you draw about renewable energy?

The net-net

As I sometimes remind myself, there aren’t ultimately all that many low-carbon energy generation sources. We’ve got solar, wind, hydropower, geothermal, and nuclear. There are other categories, too, like biomass plants or fossil-fuel-fired plants with carbon capture, but I don’t expect those to represent a significant share of future energy generation.

If wind doesn’t ‘work’ as well as people once thought or hoped – whether because parts wear out faster than expected, the financing environment has changed, or, perhaps most simply because companies can’t make money manufacturing wind turbines – that drastically complicates decarbonizing the power sector.

It’s time to get real about it. Citing supply chain issues or interest rates as the main culprit and hoping those headwinds will pass isn’t a viable strategy. Nor will it engender confidence in folks who know less about all this stuff than we do.

Reply