- Keep Cool

- Posts

- China continues to lead (part II)

China continues to lead (part II)

Did DeepSeek “deep six” the AI energy demand story?

Nick van Osdol

January 30, 2025

The newsletter in 50 words: In one fell swoop, a two-month-old Chinese startup may have rendered moot a year’s worth of hand-wringing about energy demand growth for AI. Or it didn’t. Doesn’t matter. What matters is we need clean electrons no matter what. Whether on that front or on AI, China is playing for keeps.

♡ If you find this work valuable, you can support it here. I put a lot of time into it. ♡

OPINION

My subject line for Sunday’s news roundup, “China continues to lead,” which didn’t focus much on the below, was timely. That newsletter was more about how China continues to lead the rest of the world in cleaner energy deployment, as it did again in 2024, has for years, and likely will for many years.

This week, China also has people questioning whether its leading on AI. Late last week, a Chinese startup purportedly founded around two years ago (December 2023), DeepSeek, released an OpenAI / ChatGPT rival called ‘R1’. Allegedly, it cost less than $6 million to train (a fraction of what U.S. competitors companies spend training models) and is more efficient in terms of computation capacity. To boot, DeepSeek also open-sourced its entire code base for free online. In short (I speak no Mandarin), it said “出招吧.”

Investors, analysts, and stakeholders across sectors ranging from utilities to power generation and real estate spent all of 2024 beating the drum about how much energy, infrastructure, and capital investment AI would require. There was a tireless parade of massive investment announcements, such as Microsoft, Blackrock, and others combining forces on a $100 billion effort to build data centers for AI and source sufficient (ideally cleaner) power for them.

So much so that many of the best-performing public equities were semiconductor manufacturers like NVIDIA, next-generation ‘power plays’ like advanced modular nuclear fission reactor startups, and even utilities—traditionally viewed as a relatively ‘boring’ asset class to own. Through September last year, they were the top-performing S&P 500 asset class, as they were seen as a derivative beneficiary of the AI energy-demand boom.

Gee, I wish someone had written a lengthy treatment of whether all that hoopla was overblown.

No, I’m not here to toot my own horn too much. But on December 20th, I did muse:

...efficiency gains across the data center hardware and software stack may temper the higher end of data center demand growth forecasts considerably. The corollary I’ll draw is every past red flag that’s been raised about copper, lithium, or oil shortfalls. What invariably happens when demand for a commodity materializes is that we find new ways to accommodate it. The world has never run out of a commodity; when demand spikes, new supply usually ‘magically’ materializes…

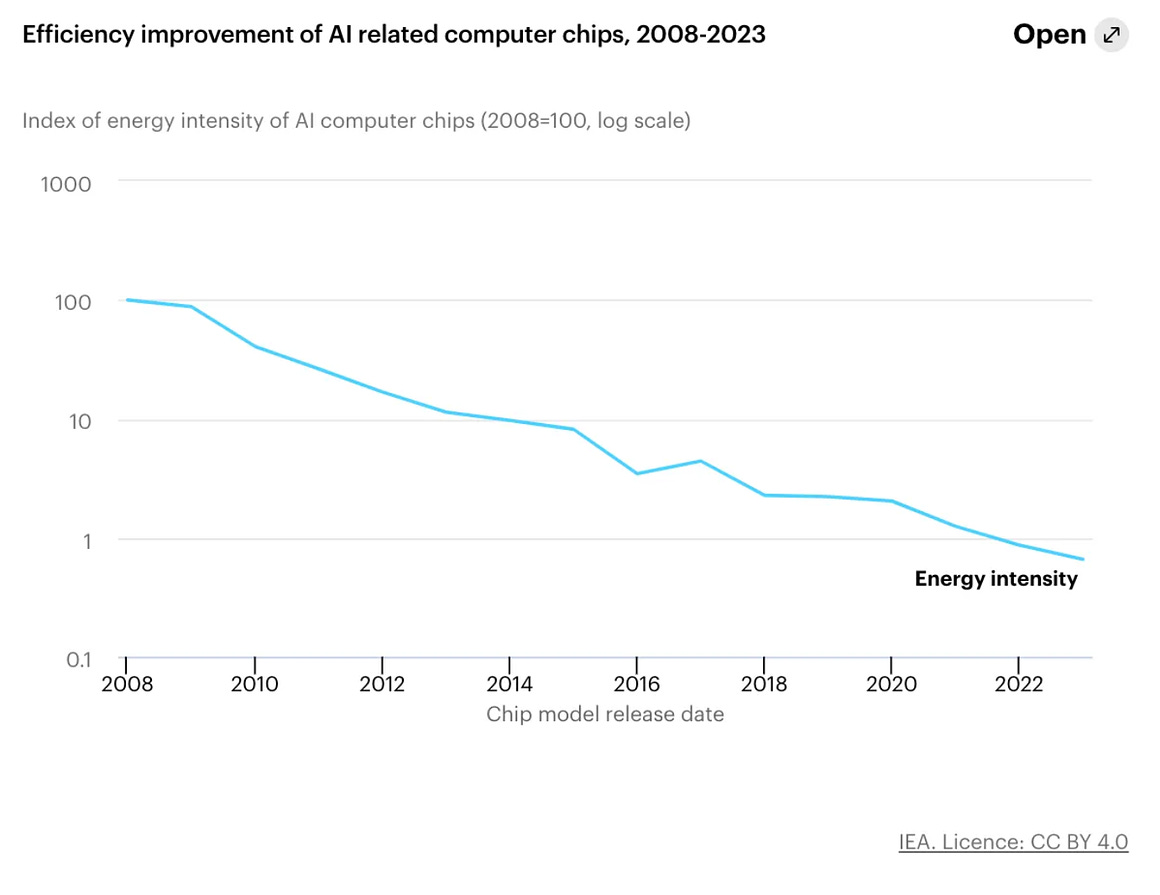

It’s not like it was impossible to see this coming. As I noted in the same piece referenced above, AI chips have already improved 100x in terms of efficiency in the past ~15 years.

Still, as people began to unpack the implications of DeepSeek, the new Chinese AI startup, markets reacted violently at first, with all those companies that previously benefitted from the AI-hype train getting hammered on Monday (NVIDIA lost $600 billion in market cap in a day, a new record). Power generation companies and utilities lost a lot of value, too:

Let’s not get too hasty, either, though. First of all, a healthy dose of skepticism of data that comes out of China—whether government or otherwise–-has long been warranted. For example, maybe DeekSeek is downplaying what it spent to build its models big time; who’s to say for sure? Secondly, markets bounced back on Tuesday, and doing tea-leaf reading based on the day-to-day stochastics of the stock market is one of the worst imaginable uses of anyone’s time anyway. †

Then, analysts spent the middle part of the week trying to patch things up. An article in the FT covered how analysts were quick to downplay DeepSeek's impact, highlighting that while it might be a problem for companies like OpenAI, which is basically a layer on top of NVIDIA chips, it’s not a problem for NVIDIA (DeepSeek spent $500M on NVIDIA chips). The source for all this is here (there is a paywall).

Other analysts unearthed a relatively esoteric concept to reassure themselves that they didn’t waste a whole year building a thesis on AI-driven energy demand. Jevon’s Paradox states that sometimes, as tech gets more efficient, we use more of it, not less. Both Morgan Stanley and JP Morgan analysts were on the beat and referenced the paradox, while Google searches for it went parabolic.

Further, plenty of developers are proceeding with business as usual despite the possibility that data centers may become much more efficient. Two days ago, Chevron and Engine No. 1 announced a partnership to build up to 4 GW of data center capacity (that’s a lot!!) powered by natural gas, not renewables. Not ideal.

Here’s my big, trenchant, insightful, and salient (™) point #1: Predicting the future is really hard. Whether it’s forecasts for when coal demand will peak or for how much solar the world will deploy in any given year, analysts who get paid to study this stuff all day long are wrong far more often than they are right. As I wrote for The Morning News at the end of last year:

The only prediction I can confidently make is that most predictions will be wrong. The most important things that happened (or didn’t) in 2024 were ones prognosticators got wrong. Trump won the popular vote! Global solar deployment beat even the rosiest estimates for the 20th year running!! Say it with me: We don’t know what’s gonna happen.

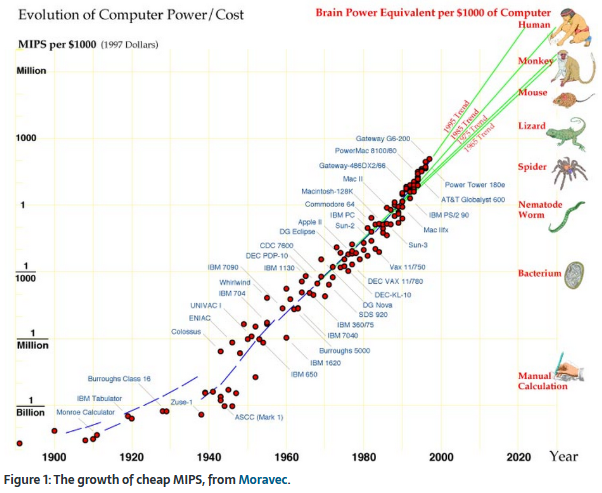

Note: This is not always true. Interestingly, some decade-old forecasts for exponential improvements in computational power themselves continue to be reasonably on track (h/t Lyn Alden):

Go long, not short

Great, Nick, you might be saying. In a world where my predictions are more likely wrong than not, what do we do? First, I’d caveat my bold statement by saying that, as I wrote on Thursday, there’s a lot of value to leaning into areas of investigation or domains where you have expertise or at least have sufficient curiosity and capacity to pursue it and build it. The people who make the best bets about the future have some combination of a) incredible insight, b) incredible luck, c) incredibly privileged access to insider information or people that satisfy category “a or c” and share it.

Evergreen advice in many cases (tweet link here)

If, like me, you are not one of those people, betting on (or choosing a career or making life decisions based on) longer-term trends versus short-term hype cycles tends to help. There’s a term here called the Lindy effect that basically says the longer something has been around, the more likely it is to stick around. The investment boom that’s contingent on the idea that AI will require unparalleled amounts of energy has been around for a year, maybe 18 months, at least for the mass market.

That’s not very long.

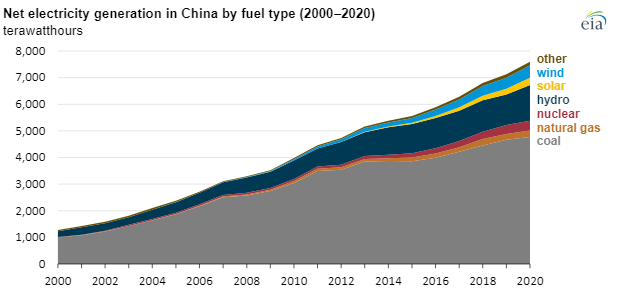

What do we know longer-term? Well, for one, we do know that demand for energy goes up. Take China as an example, given a lot of this newsletter is about it. Electricity generation in China has risen almost eightfold since the turn of the century:

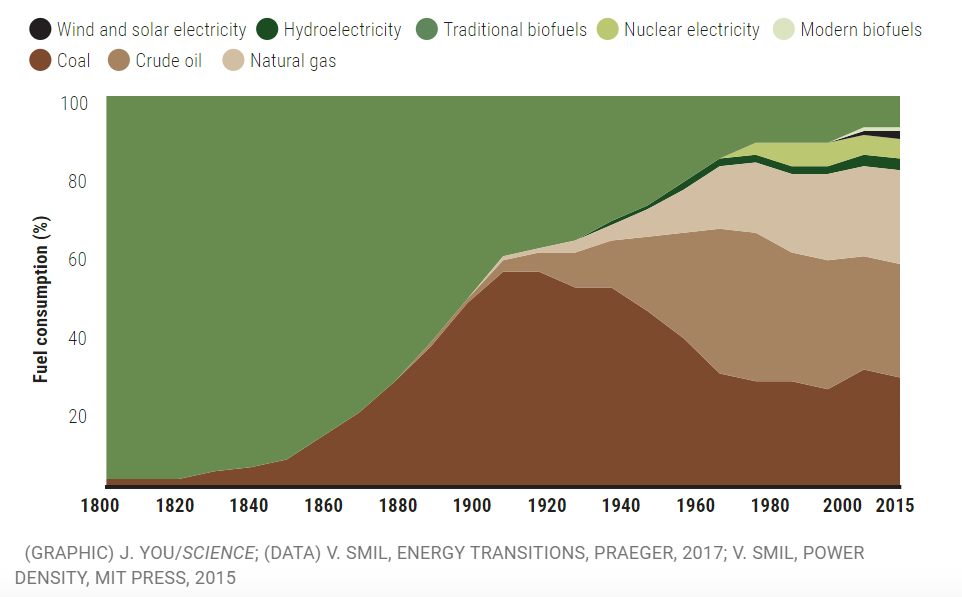

Much longer-term, we also know that energy transitions do happen, even though they take time. The world used to produce almost all its energy by burning wood. Suffice it to say that’s no longer true, though we do still burn a lot of wood!

With respect to China (or the world), signs of a ‘true’ 21st energy transition may be kind of hard to see when you zoom out to global greenhouse gas emissions and coal usage that are at all-time highs. Still, the fact that I titled this piece “China continues to lead…” is not a mistake. I say that even while, as shown in the previous chart of how Chinese electricity generation has grown, it is still predominantly reliant on coal (more than half of the world’s coal, in fact). China is also the world’s number one greenhouse gas emitter and has been since 2006. 90% of global carbon dioxide emissions growth since 2015 came from China alone.

What can be simultaneously true is that China may someday surpass the U.S. as the largest cumulative emitter of carbon dioxide emissions since the Industrial Revolution (so far, the U.S. is still number one) and that—alongside trouncing the U.S. on things like AI—China is genuinely serious about decarbonization and the energy transition. As we started with, they routinely beat all other countries in clean energy deployment. They’re leagues ahead of the rest of the world on EVs, whether in manufacturing, sales, EV charging infrastructure (see here, too), or even trying alternative approaches that get little play elsewhere, like battery swapping. China also seems modestly serious about decarbonizing heavier industry; they have targets to reduce emissions from steelmaking (the technology for which exists), even as they produce half the world’s steel and use a lot of coal today to do it, and even as it’s a harder hill to climb than building new solar.

To quote Jayati Ghosh, an Indian development economist (instead of a white man for once):

...international action on climate would require trust. At the moment, there is zero trust, and the G7 has zero legitimacy. The rest of the world is saying to the rich countries, If you guys are not going to do anything, we’re not going to do anything. It’s completely counterproductive, but that’s the way it’s going — other than in China, which saw decarbonization as the future, and therefore invested heavily in it.

Whether in AI or decarbonization, China seems reasonably agnostic of outcomes other than gaining a material geopolitical advantage and improving the lives of its populace. Hence, I’m not convinced they necessarily “care” that much about greenhouse gas emissions, though reducing air pollution from burning coal is definitely beneficial for its citizens.

But if China is investing heaps in cleaner energy research and development, manufacturing, and deployment—in the same way they aren’t resting on their laurels with respect to AI—it’s safe to assume that they see economic and technological benefits to doing so.

That’s my big, trenchant, insightful, and salient (™) point #2: If China’s doing it, it’s for its own benefit. It’s not for international climate targets or to play nice with the rest of us.

Why China’s seriousness matters

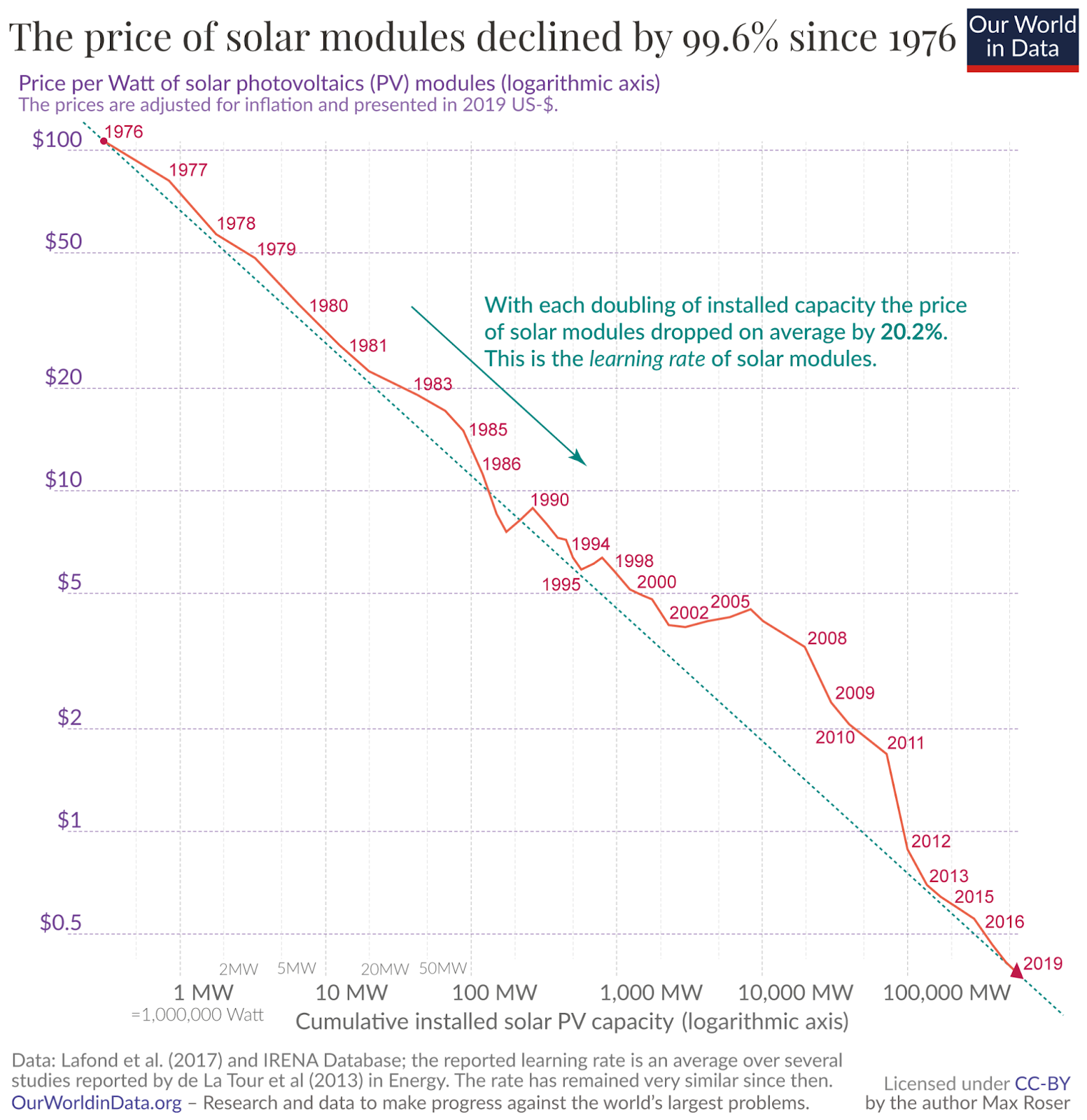

Which brings me to why I think China’s leadership on many pillars of the energy transition matters. What they see in, say, nurturing a domestic manufacturing base and building and deploying solar, EVs, and battery energy storage extends beyond a desire to own the world’s supply chain for panels and batteries or to sell their wares to the world. I reckon they see useful technologies that are backed by long-term trends (which, again, we’re more interested in here than short-term ones). Like computer chips for AI, solar and batteries have been getting much more efficient for decades (long-term trend!) and offer flexibility and speed to deployment.

Other technologies and generation assets, especially in the U.S., are hamstrung by supply chain issues (say, transformer backlogs), infrastructure development costs, or the previously centralized nature of the power grid and the relative difficulty of expanding transmission and distribution line (transmission and distribution costs as an overall portion of electricity costs have risen continuously for years), and finally, with a nod to nuclear fission, regulatory factors. Those are all theoretically tractable issues, but there’s no inherent indication they’re going away soon.

Note the growth in delivery costs versus power production here; bigger bottleneck!

In the future, whether it’s data centers, desalination plants, or some other big power hog, expect to see a lot more energy generation purpose-built to serve the plant or facility and bypass the grid altogether. With all aforementioned constraints, there’s a lot of value to power generation (and consumption) that’s off-grid.

Build it, and they will come

So, should we stop worrying about whether AI will hoover up a boatload of electricity now that there’s an indication efficiency gains will render a year’s worth of hang-wringing moot?

No. Big, trenchant, insightful, and salient (™) point #3 is: We need more clean electrons no matter what. Who cares whether it’s for data centers? We need it to reduce power sector emissions, desalinate water, make more steel in electric arc furnaces instead of blast furnaces, charge EVs, or whatever else your preferred use case is. To reiterate that I’m not betting big on any singular predictions or trying to make them, I don’t care whether you believe more in advanced nuclear fission, fusion, solar and batteries, or something else. I personally wouldn’t put my ‘chips’ (get it) all on one generation source, and certainly not on one source of demand, like AI. For one, there’ll likely be a mix of energy generation assets for a long time. Secondly, as is true today, it will vary considerably by region. Here’s Adam Tooze on that front:

Energy transitions are not so much a general historical phenomenon, or societal regularity, so much as a sectoral and regional particularity dependent on technologies and complex and long-lasting investments in infrastructure. The displacement of biomass by coal and the rapid displacement of coal by electricity, oil and natural gas in US domestic and commercial uses, is a case in point.

Adam Tooze

Still, the point remains: Wherever they come from, we’ll need more clean electrons.

The net-net

Don’t be a two-year trend surfer. Be a twenty or 200-year surf rider! It’s a more ‘sustainable’ wave to ride. To re-iterate, the longer-term trends we identified today include:

Short-term, people often freak out about whether a new technology will require insane amounts of energy or raw materials to produce

Forecasts (in general and with respect to the above) are more often wrong than right

Medium-term, technologies like solar, batteries, and computing chips have a strong track record of continuous improvement

Long-term, demand for and use of energy will keep going up

Longest-term, energy transitions do happen

My last big, trenchant, insightful, and salient (™) point is that individuals, organizations, and entire countries that position themselves with the above in mind are likely to be successful, though how you measure success matters a lot.

And, not that I or perhaps anyone really has his ear, if there were anything that could get Trump and his Administration to say, at minimum, maintain some policy support for things like building out domestic battery and solar manufacturing, considering all of the above (and following him around with a tuba-like instrument that blares “Don’t let China beat you!”) might (?) help. With respect to the Chinese startup and its AI model, he did say U.S. companies needed to keep “competing to win.” We’d all do well to understand that’s as true about energy as it is about AI.

Ciao,

— Nick

† As an aside, your brain is still the most powerful large language model by an incomprehensible margin. Feed it good information and take good care of it, and it’ll surprise you.

Reply