- Keep Cool

- Posts

- Boring Capital

KEEPING COOL WITH

Hi there,

New month! April is a big month for us here at Keep Cool, and not just because Gabe is getting married and because the weather is turning in New York. April is a big month for us because we’re excited to roll out something new. Glassdome, a company laser-focused on accelerating sustainability in manufacturing and industry, is our first-ever Presenting Partner. Over the month, you’ll get to know Glassdome deeply across our coverage and will have the opportunity to connect directly with their team if and where it makes sense to do so.

I’m excited about this partnership for the following reasons:

Clear value proposition: Glassdome is a great company with a conscientious team I've learned a lot from. I'm excited to explore why I'm excited about their work with you.

Connective tissue: As with any presenting partnerships we’ll take on, I'm confident there are lots of ways Glassdome’s work can be accretive to people and companies (maybe you and yours?) in Keep Cool's orbit.

Content alignment: Glassdome's work is well-aligned with one of my content pillars for 2024, namely decarbonization and sustainability in industry and manufacturing.

Setting the foundation: As we announced a few months ago, Keep Cool is once again independent. Partnerships like these allow us to sustain the brand and establish new ways we amplify meaningful work. If you find the format valuable and think your organization would be a good future partner, respond to this email and we’ll discuss.

So, what can you expect this month? Lots of content, as usual, for one. You'll get two great deep dives on Glassdome specifically, which will integrate discussions with the team as well as a variety of their customers and stakeholders in their ecosystems. You'll also get a more narrative-led podcast that hits home some of the storytelling that doesn't always jump off the written page. Plus, you'll have lots of other touchpoints with Glassdome to explore their work.

Of course, there'll be no shortage of other content this month. But you'll likely note that a lot of it also builds on top of Glassdome's focus on making the future of industry and manufacturing 'work' for all stakeholders, including the Earth. I'm looking forward to it – more to come soon.

The newsletter in 50 words: Climate tech venture capital, and venture capital in general, are sexy. However, other components of the capital stack, particularly on the private equity and infrastructure side, are arguably the more (and perhaps most) important capital pools in climate tech and energy transition work right now.

SPONSORED BY GLASSDOME

Do you work with manufacturing companies? Use their products in your supply chain? Are you part of a manufacturing or industrial organization yourself? Glassdome is a company you should know about.

Glassdome works with major global manufacturers like SK to help them calculate product carbon footprint and build a sustainable, competitive edge for their businesses. This matters from a regulatory compliance perspective as new regulations like the EU’s Battery Regulation and Carbon Border Adjustment Mechanism mandate product carbon footprint calculations for imported products (and enshrine a lot more complexity, too).

Glassdome's technology measures and manages the carbon footprint of products based on data that isn’t estimated or based on averages, making it one of the most high-fidelity and transparent sources of truth.

Want to sponsor Keep Cool? Click here.

OPINION

Something funny happened last week. I noted I joined Climate Capital as a Venture Partner. Many of you wrote in to say congratulations. Thanks for doing so! What I was really surprised by was just how uh, horny, for my little announcement the Twitter and LinkedIn spheres were. I got way more engagement on those posts than on any of my harder hitting climate tech analysis or even my memes. Which is all well and good, I can take the atta boy and not deprecate myself here.

Still, I do find it a touch funny how gaga for venture capital many of the circles I swim in are. My friends that spend their time playing billiards in Brooklyn pool halls or sub in on bass at small punk rock shows are just as cool as my big shot venture capital friends. Ok, maybe that’s not the right analogy. What I want to discuss today is that, in many ways, venture capital is not the most important component of the climate tech capital stack. All components of the stack matter, sure. But as I often discuss when a specific sub-area within climate tech is underloved, other types of capital deserve more love, too.

Boring Capital

Let's start with an example. On the most recent episode of the Keep Cool Podcast, I interviewed John Skrinar, Partner at Cresta Infrastructure Management, an Infrastructure investment firm. We hit on a lot of things, and you can check out the full episode here (and Plus subscribers can read a full transcript here), but here's one portion of the conversation that stood out to me specifically:

We're looking to invest in pretty boring things? We make really stable investments in infrastructure… the infrastructure that we need for energy transition. This portion of the market is gaining momentum.

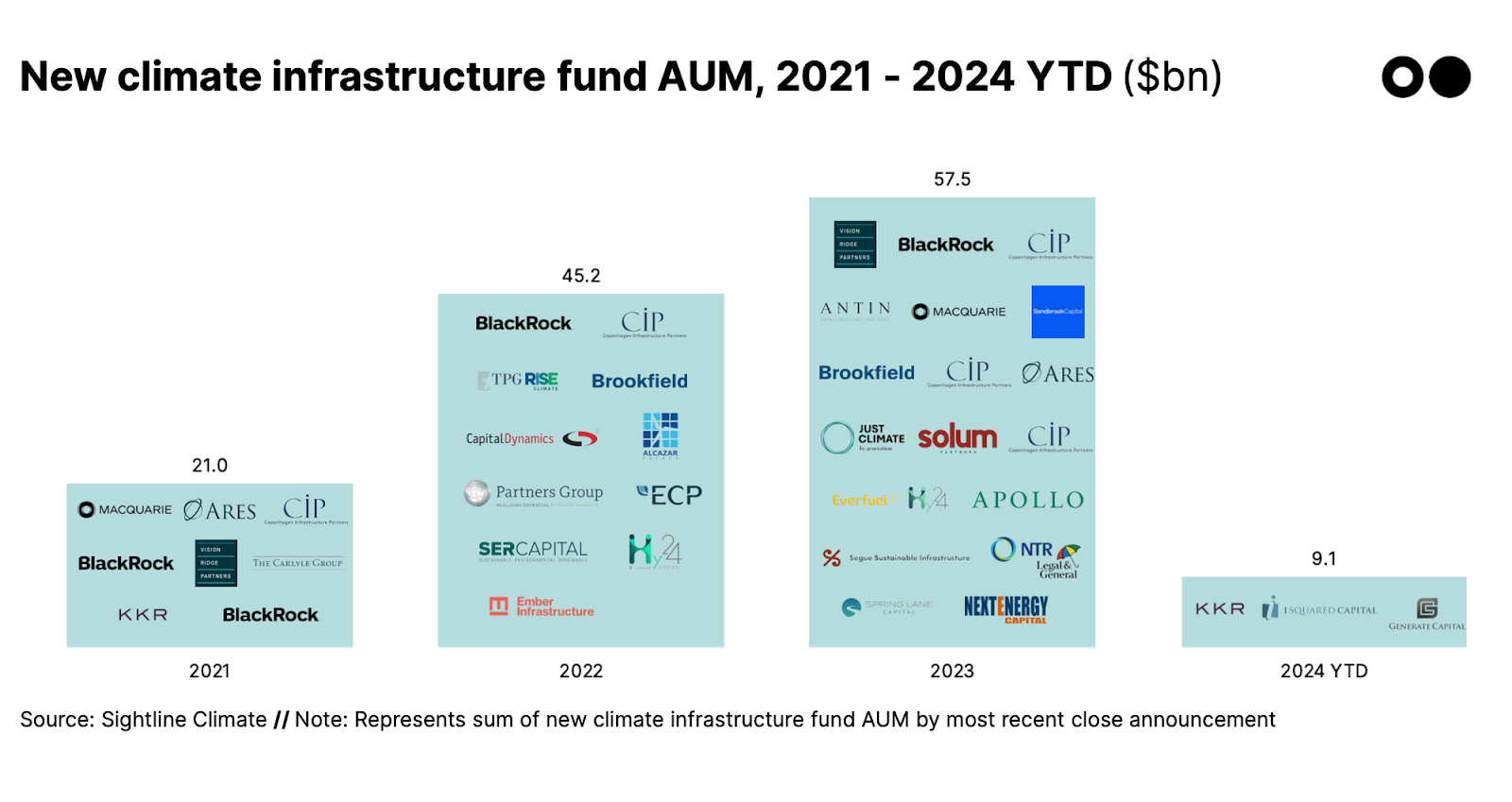

I'll give you one anecdote. When we made our investment in LF Bioenergy in 2021, most of the participants from a financial sponsorship perspective were strategics or utilities. It was Dominion, it was DTE, it was BP and Shell. I don't know of too many private equity firms that were investing in RNG on the dairy side back in 2021. As you walk into 2024, we see teams backed by Warburg Pincus, BlackRock, ECP, Ares… These are really big private equity firms with tens of billions of dollars in their management that have moved into the space and are saying, hey, look, we're okay with these risks. And that happened in a three-year period.

It's promising to see this 'boring capital' move into climate-focused tech and energy transition infrastructure. It's one of the things I find most encouraging in energy transition dynamics right now. Once you've shifted to a state where a lot of the work that needs to get done is a little bit more boring, as opposed to needing to be completely cutting-edge, well, that’s good!

The 'boring' capital we're discussing entails different risks than venture does. That's a critical point because it means, right now, there are actually things to invest in that are at the level of maturity needed for the 'boring' capital to get interested. That maturity level also often correlates with more impact – whether measured in emissions reductions or another variable you care about. Climate Tech VC has done an excellent job of characterizing the size and shape of the new entrants (below). Still, I think the point is worth iteratively hammering home.

For examples of what ‘boring’ capital invests in, John offered several. Cresta invests in manure management projects on dairy farms that reduce methane emissions by generating renewable natural gas (the project John referenced in his quote above). Cresta invests in green hydrogen projects. Cresta invests in carbon capture. I imagine if the DOE-backed projects that we highlighted last week are successful, Cresta will fund that type of work in the future, too.

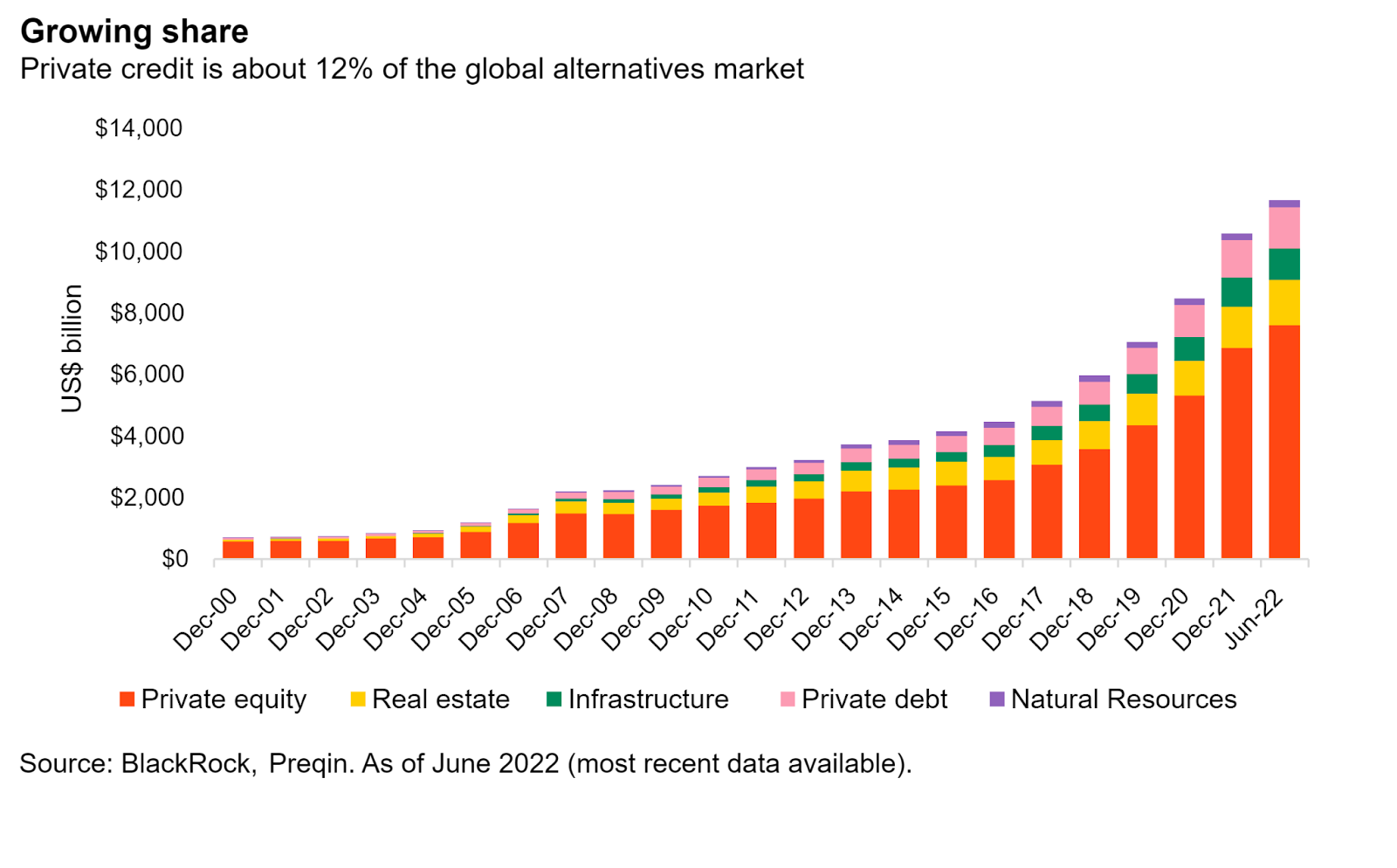

It’s also worth noting that the more ‘boring’ capital pools we’re talking about dwarf the size of venture capital. Sure, some of that makes sense based on the role this pool of capital plays. Still, the numbers themselves can be staggering.

Globally, there are roughly $2.5T in venture capital dollars under management. Compare that to more than $6T in private equity in the U.S. alone, alongside ~$1.2T in private debt (see above). Globally, private equity is about a $13T market. For even further context, the global natural gas market, for instance, is worth $300T+.

Again, at the risk of being overly repetitive, different financial pools, like venture and private equity, play very different roles. And the natural gas market size noted above is for the entire market, which is a quite different measure than measuring PE and VC AUMs. Still, hopefully, this perspective is a bit eye-opening. Spending all our attention and time on the venture capital pool wouldn’t get us particularly far down the greenhouse gas emissions curve.

Other (dirty) money

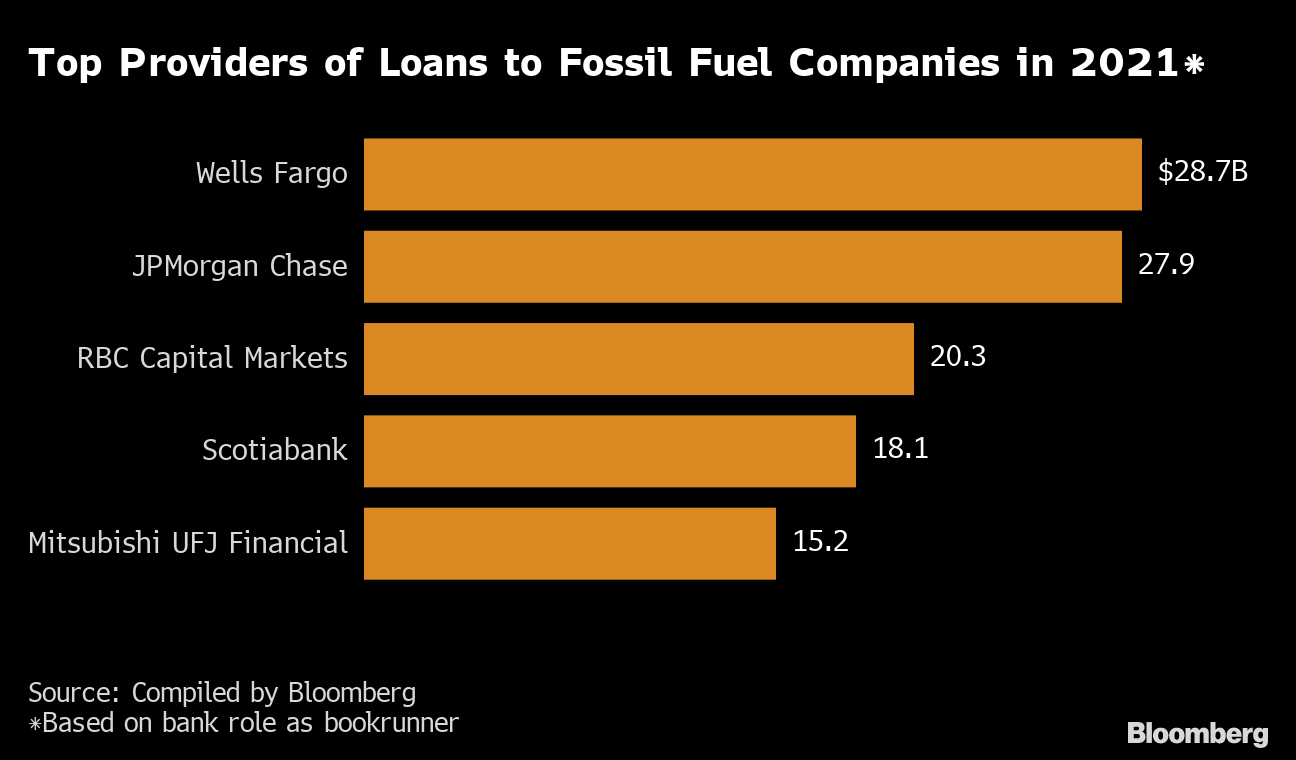

There are other components of the climate tech capital stack that are, from my vantage point, often just as salient as venture capital. Take, for instance, bank lending to oil and gas companies. You can count on a (somewhat) heartening headline every time a new bank notes it won’t finance new oil and gas projects or lend to new greenfield oil exploration projects. When that happens, it’s good!

Still, most of the world’s biggest banks continue to make lots of money lending to oil and gas companies. More than half a trillion dollars gets lent to oil and gas companies annually, even if that number is declining. Even those banks that aren’t doing new lending often still lend to existing clients and projects. In a world where venture capital gets all the love, lending and other types of larger capital pools really make the world go round. It’s just not the world that gets discussed on Twitter and LinkedIn.

An oilsands operation in Canada, i.e., the type of massive infrastructure many banks still finance (Shutterstock)

Many of the biggest banks in the world, like Wells Fargo and JP Morgan, continue to finance new oil and gas projects, ranging up and downstream and from brownfield to greenfield projects. While not the biggest pool of capital, the future emissions this funding enables, unfortunately, dwarfs the emissions avoidance or mitigation potential of lots of other capital pools. When Diamondback and Endeavor merged earlier this year, they estimated they will produce 800,000+ barrels of oil and oil equivalents daily. When burned, that equates to ~400,000 tons of CO2-equivalent emissions, also daily.

Private credit lending to oil and gas companies is also growing. $9B was lent between 2021 and 2023, compared to $450M in the two years before that.

The net-net

Venture capital is hard to compare to other pools of capital. It’s romantic in that it involves many distributed bets on ideas and dreams. Tesla was venture backed and, in my opinion, alone accelerated decarbonization of transportation by 5-10 years. Still, Tesla wouldn’t have survived without government loans either; the company almost went under twice. And it’s been a big beneficiary of other ‘boring’ capital pools as it has matured.

Suffice it to say, the world would stop without boring capital, and efforts to really reduce global warming can’t get started without it. As it pertains to my work, don’t get me wrong, I’m quite excited to wear the venture capitalists hat, too. But in writing this piece I was reminded that the media and consulting work I do is just as important too. Even if it isn’t as glamorous. It takes all kinds of kinds.

CAMP KEEP COOL

Last week we shared an exciting announcement about our first flagship event, Camp Keep Cool. ‘Camp’ is a highly vetted retreat for climate and energy entrepreneurs, founders, CEOs, and operators taking place in the heart of the Rocky Mountain Wilderness. Starting and operating a company is lonely. You have to make difficult decisions with imperfect information on problems you’ve likely never faced before. Camp was started because we know the best way to overcome the challenges is to learn from the wins and mistakes of others, and to surround yourself with those who’ve been there, done that.

Whether you’re in the thick of it in decarbonization or you’re a biodiversity founder, finding and connecting with your people is tough. But when you do, it’s life changing. And that's what Camp is for.

If attending this sounds interesting to you, please reach out and drop us a line. We are only going to build this if its something the community wants to be a part of. Respond to this email, check out our landing page, or apply to join today.

Hasta la vista,

– Nick

Reply