- Keep Cool

- Posts

- An untapped market for adaptation

An untapped market for adaptation

Why solar radiation management is an opportunity for the private sector

Nick van Osdol

November 26, 2024

Hi,

We’re sending on Tuesday versus Thursday this week to respect the Thanksgiving holiday in the U.S. (and elsewhere). Hope you enjoy the time, if you celebrate.

Today’s note builds on our recent coverage of geoengineering. Science communicator Andrew Lockley, also an independent geoengineering researcher, drafted this piece with LLM support, offering insight into and opinion on the unique opportunity and need for the private sector to accelerate study and scalability work in solar radiation management. I (Nick) extended, edited, formatted, illustrated, and added color. Let us know your thoughts by responding to this email.

To hear more from Andrew in the future, you can join 2,000 others who subscribe to the Carbon Removal Updates substack here.

The newsletter in <50 words: Solar radiation management represents an untapped opportunity for decisive impact. Private capital will need to participate, fueling the innovation that can drive a more resilient future.

OPINION

Trump is here. The game has changed. Any climate solutions proposed now have to be compatible with the new political reality.

Mainstream climate solutions involve not eating burgers or flying, and such proposals get a bad rap from the libertarian right. JD Vance claimed, “They want you to live in a pod, eat bugs and own nothing.” But ideology can't trump reality—Trump or no Trump—because physics isn't negotiable. How, then, to avoid climate breakdown?

Even before the U.S.'s recent political shake-up, solar radiation modification (SRM) geoengineering was looking increasingly necessary as a potential gap-filler. It has the potential to keep us cool while the world works to reduce emissions and scale carbon removal. Even SRM's sworn enemies—and there are many—must concede that 1.5°C is surely dead without it, and 2°C likely is, too.

That need for SRM translates into investment opportunities. This has only grown more compelling, with an expected evisceration of the U.S.'s federal funding for energy transition work and the removal of many environmental regulations.

Climate solutions are urgent and varied, but current mitigation and emissions reduction strategies alone are far from sufficient to keep pace with escalating risks:

Considering both historic and future committed emissions, carbon dioxide removal (CDR) is an essential solution, as the Earth will continue warming even when greenhouse gas emissions globally fall, given carbon dioxide’s atmospheric lifetime and the accompanying loss of aerosol cooling. At the same time, even rapid mitigation and scaling of carbon removal will not control the risks inherent to the world’s current warming trajectory. Nor can it prevent other ‘tipping points’ that could amplify climate change and damage.

Even COVID-scale economic changes won’t arrest fossil fuel usage sufficiently quickly. IPCC projections illustrate the scale and scope of this gap, as do countless other recent reports, including the EU Climate Action Progress Report 2024:

“To limit warming to the 1.5 °C Paris Agreement temperature target, secure a liveable future for all, and avoid the worst impacts of climate change, global greenhouse gas emissions should fall by 43% below 2019 levels by 2030 and by 84% by 2050.”

That 43% reduction in emissions simply isn't going to happen, absent some crisis that dwarfs COVID in economic impact, as 2030 is only five years away. Interventions like solar radiation management (SRM) now deserve serious consideration.

Why SRM, why now?

SRM’s approach is both ambitious and straightforward. It entails reflecting a portion of sunlight back into space to cool the planet. This isn’t without precedent. Large volcanic eruptions (e.g., Pinatubo in 1991), as well as sulfur dioxide emissions from shipping fuels, show aerosols yield measurable cooling effects. SRM seeks to harness this cooling potential intentionally. It doesn’t address emissions, air pollution, or land use change, but it offers a stopgap, potentially alleviating immediate climate stresses, while CDR and other technologies scale.

The potential of SRM is clear: It could offer relief from peak temperatures and associated climate risks. Time out from these peak temperatures is what humanity needs for orderly energy transition and many other ‘wedges’ of decarbonization.

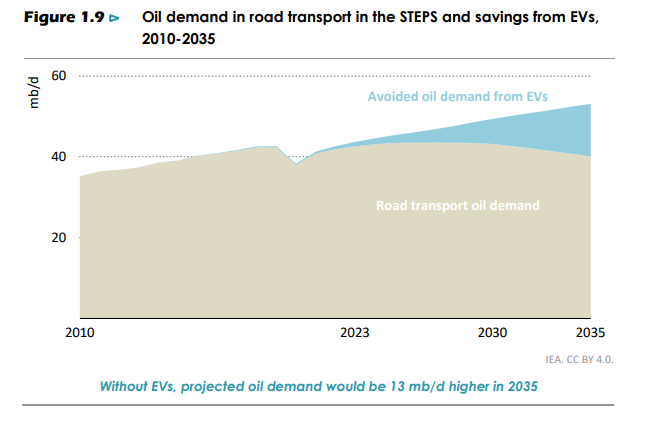

Oil demand, for example, may soon peak globally. However, a peak in demand is not the same as a meaningful reduction; past, current, and future emissions are an enduring problem due to carbon’s long atmospheric lifetime. Projections for decreased oil demand globally over the next ten years are not sufficiently drastic. While these projections may be too pessimistic, and EVs are displacing some oil demand, it’s not fast enough.

Source: The IEA’s World Energy Outlook 2024

Absent a wholesale abandonment of developed world lifestyles, these transitions take time. You have to build factories, then manufacture cars, then sell them, and hope others will build commensurate EV charging infrastructure. None of that happens overnight; the shift to EVs, replete with significant subsidies from many global governments, is entering its third decade. And every other wedge needs to follow this pattern.

Despite the need to buy more time, SRM remains chronically underfunded and under-researched. It receives a negligible amount of climate research funding, in contrast to billions poured into carbon removal, which has yet to offer meaningful evidence that it will contribute significantly to net-zero efforts (but it does have plenty of potential, particularly in the long-term and for much-reduced residual emissions).

Hence, there’s a unique opportunity for the private sector to step up, especially given that the early movers in SRM could help shape a market with at least some private sector demand, as seen in the (still quite young) carbon removal industry. Companies like Make Sunsets and Stardust are advancing limited stratospheric aerosol injection trials (‘SAI’), while aerospace leaders like SpaceX and Dawn Aerospace have the technology to support SRM initiatives, whether their customers are state or private sector.

SAI is the best-studied and most technically feasible SRM approach. Yet, it still requires high-altitude aerosol dispersal technologies that don’t yet exist at scale. While these challenges demand investment, they also represent cross-sector opportunities. Innovations like reusable rockets, rotating detonation engines, and hypersonic vehicles are already making strides. Private capital could help narrow existing gaps.

Beyond deployment, SRM both demands and accelerates related technologies: real-time climate monitoring, AI-driven modeling, and advanced flight systems—all of which are avenues that can drive returns on investment, regardless of whether SRM is deployed at scale or not.

Learning from other proactive, precautionary investments

We’re no strangers to technologies built as safeguards rather than for immediate use. Building out SRM capabilities doesn’t mean rushing it into deployment; it means preparing responsibly for the future. Examples of technologies with a “just in case” role abound, and many have become common infrastructure all around us.

Flood barriers are a good example. Major cities worldwide invest billions in these defenses, not because they face floods every day, but to prevent catastrophic damage in case of a rare, severe storm. In the U.S., flood control is part of $15+ billion in federal funding for disaster preparedness and mitigation. Similarly, most fire protection systems aren’t ever activated. Yet, they offer security, reduce risks, and often pay for themselves, whether measured by insurance savings and / or public safety cost-benefit calculations.

A storm surge barrier bridge in the Netherlands designed to protect against rising sea levels (Shutterstock)

In the same way, SRM could act as a climate “fire protection system”—only deployed if and when circumstances call for it, whether sponsored by government funding, philanthropists, or the private sector. The idea isn’t to commit to SRM deployment tomorrow but to ensure it is deployable in a controlled manner if and when needed. Like NASA’s DART mission for asteroid detection and interception, this is a matter of readiness, resilience, and ensuring we have the capacity to respond if a critical need arises.

The regulatory balance

Initiatives like the 2024 American Geophysical Union (AGU) guidelines bring ethical oversight to SRM research, emphasizing transparency and accountability. But there’s a fine line between enabling safe innovation and over-regulating a nascent field. A great example of the latter is the U.K.'s ham-fisted regulation of nuclear power, which has significantly raised deployment costs. While Non-Use Agreements ostensibly aim to prevent misuse, they risk inadvertently stifling the competitive, diverse research environment needed to develop SRM responsibly (which is arguably their intention). When innovation is restricted, we collectively lose out on advancements that can make SRM safer, more efficient, and more available to meet future global needs.

Consider the role of regulation in other critical areas. The U.S. energy sector, for instance, saw decades of regulatory delays slow the development of nuclear and grid modernization projects, limiting resilience and responsiveness. Conversely, in times of urgent need, private-sector leadership, coupled with public-sector support, has propelled innovation. During World War II, private firms scaled production to meet military needs. During COVID-19, the rapid development of vaccines by pharmaceutical companies—backed by advanced market commitments–demonstrated what a supportive regulatory environment can accomplish. SRM, with a balance of oversight and freedom, could follow a similar trajectory of rapid, responsible advancement. Notably, in both listed cases, private sector companies also made a lot of money, ultimately supported by government spending.

The net-net: A distinct role for the private sector

The private sector’s involvement in SRM isn’t just about funding. It’s about fostering a framework for SRM that prioritizes competition, transparency, and accountability, all of which are needed to earn and maintain public trust. Through funding independent research and by supporting trials, the private sector can build an SRM field that’s at least grounded in real-world data and ideally integrates ethical considerations as well.

A balanced SRM technology market—one shaped by competition, innovation, and stewardship—can ensure this solution remains globally inclusive. With early, responsible investment, the private sector has an opportunity to create a more resilient and flexible SRM landscape, one that avoids the inefficiency and delay of rigid, state-led dominance. Even if all Western deployments are state-funded or state-approved, the private sector will ultimately design and manufacture enabling technology—just as it does with military hardware—and will likely be responsible for operational delivery as well. The time to invest in and demonstrate these technologies is now, wrenching control of the development process away from the risk-averse and ineffective university bureaucracies, which have strangled various SRM projects in the cradle (SPICE, SCoPEx, plus any quietly buried before anyone even heard of them).

Of course, there are open questions around the geopolitics of SAI and SRM, but the ‘climate clock’ is ticking. For those with the vision and will to act, SRM represents an untapped opportunity to make a decisive impact. Private capital will need to participate, fueling the innovation that can drive a more resilient future.

You might hate the idea of SRM. But you'll likely need it, so why not make a profit from it? Maybe you should learn to stop worrying and love the spraying? The future may reward those who embrace its unfolding dystopian nightmares.

Thanks for reading, and happy Thanksgiving,

— Andrew & Nick

Reply