- Keep Cool

- Posts

- An absolutely stuffed stocking (including with coal)

An absolutely stuffed stocking (including with coal)

Last newsletter of the year!!!

Nick van Osdol

December 23, 2024

Hi there,

This will be my last newsletter of 2024 (save for paid subscribers and those of you who are most engaged in opening and clicking, who get one to two more). I’ll be working on other projects, reading, and sleeping until at least January 9th. I stuffed this one to the brim with content for you all to peruse while I’m out—complete with much more than usual for my Sunday sends, all the usual elements, too, and, as ever, a curatorial eye trained on what actually matters.

Thanks as well for the patience on the send time. I’ve been debugging my brain and body in the desert all weekend, save for one fantastic engagement party (congrats Jack & Kim)! Photo evidence that I did, indeed, get outside instead of just working the whole time offered at the end of the newsletter.

In today’s newsletter (more than usual):

One story in a (few) sentence(s) (and a chart)

Tell me some good news (for the year)

Top Keep Cool content from 2024

More exceptional content from elsewhere

Climate tech and energy headlines from the week

Climate tech fundraising announcements

THIS WEEK IN CLIMATE TECH & ENERGY

One story in a (few) sentence(s) (and a chart)

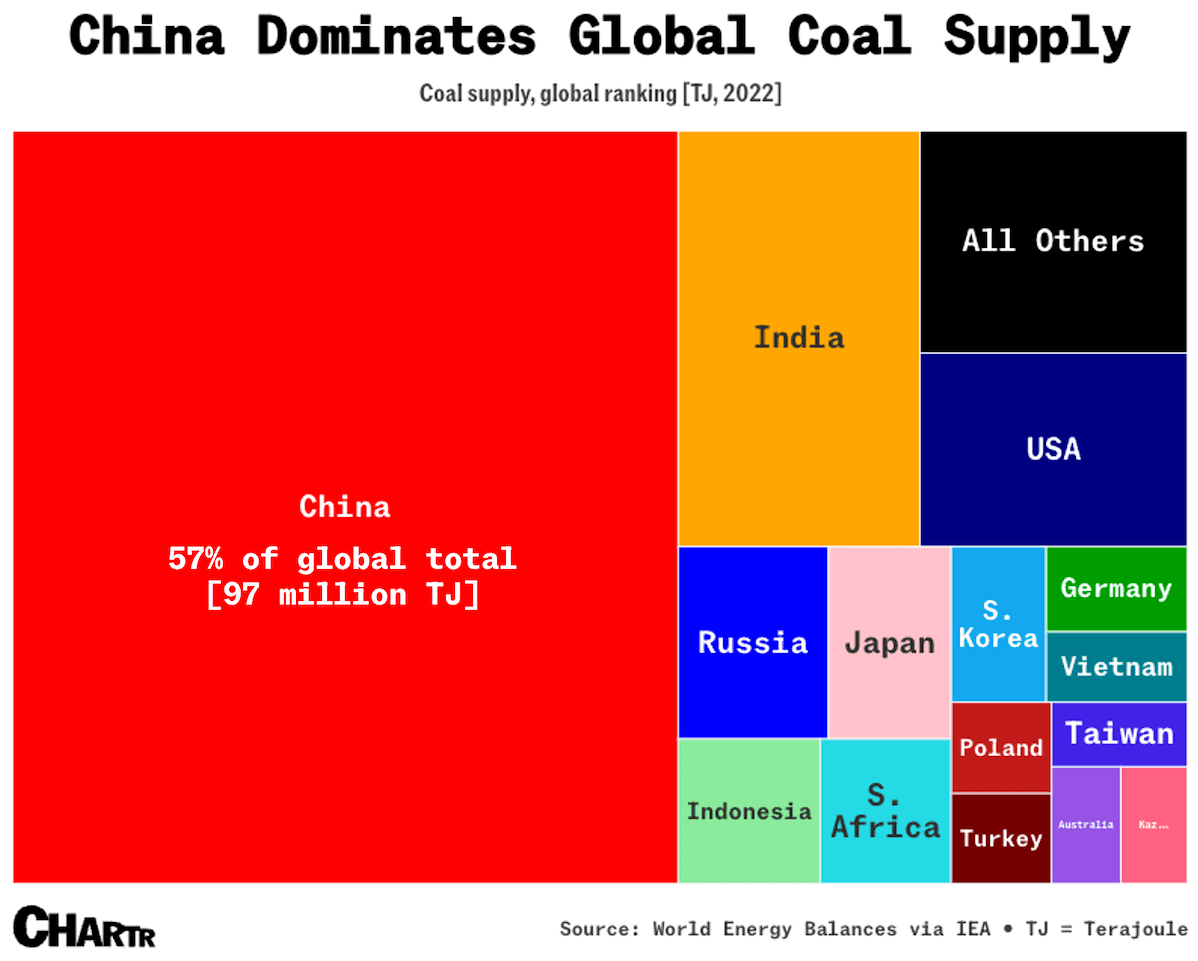

• There’s good news galore in this newsletter. Still, I want to start by emphasizing that greenhouse gas emissions, alongside coal, natural gas, and oil consumption, production, transportation, and combustion globally, will all still hit record highs in 2024. Much of this is concentrated because of continued Chinese and Indian dominance in coal production and use (as visualized below). At many local, technological, and industry-specific levels, energy transitions happen very quickly. At the highest level, things are still moving quite slowly and certainly far too slowly to meet any international global warming target. All these things can be simultaneously true, as I often say. Here’s the chart link; more on all that coal in our stockings later further along in this newsletter.

Tell me some good news (for the year)

Not intended to be comprehensive, but here are some higher-level quick hit good news items to close the year on:

• From the revival of decommissioned plants in Japan to advanced small modular reactors and commercial fusion plants committing to building and energizing reactors in the next decade (both topics covered further below with announcements, too), nuclear fission and fusion alike came back in a big way in 2024.

• BloombergNEF (BNEF) estimates stationary battery energy storage installations will cap the year out at or above 170 GWh in 2024, beating 2023 by a factor of more than two and improving on other estimates that came out as recently as October. BNEF also forecasts global solar additions to grow another ~30% in 2024, marking two decades of growth in which each year has more or less beaten forecasts. Further, according to FERC, the share of low-carbon electricity capacity additions in the U.S. in 2024 should come in at or above 90% (primarily solar). Link. Link. Link. Link. Link.

• The IEA released new projections this week that estimated the cost of “always-on” geothermal energy could fall by 80% by 2035 (to roughly ~47.5) per megawatt-hour (MWh). That’d make geothermal one of the more attractive forms of dispatchable, low-emissions electricity. Link.

• Amazonian deforestation dropped to a nine-year low in 2024, falling by more than 30%, per Brazil's National Space Research Institute. Caveat: A reduction in the rate of deforestation doesn’t mean deforestation isn’t continuing; the world lost another Delaware-sized equivalent of Amazonian rainforest this year. Link. Link.

• On the manufacturing front, a new report from the Solar Energy Industries Association (SEIA) and Wood Mackenzie heralded that U.S. solar manufacturing is back, baby: “After a record Q3, U.S. solar manufacturing has reached a critical threshold. At full capacity, American solar module factories can now produce enough to meet nearly all demand for solar in the U.S.” Link.

• Contrary to many media headlines that intimated otherwise, across almost all markets, global EV sales will have grown again in 2024, especially outside North America. Continuing the non-North American trend, countries from China to India, Pakistan, and Brazil all deployed record amounts of lower-carbon energy this year, too. For context, China deployed four times more wind, solar, and other renewables in 2023 than all other G7 countries combined. Link. Link. Link. Link. Link.

• Methane-reducing feed additives for livestock and their methane emissions from enteric fermentation, like Bovaer, which was approved in the U.S. by the FDA as well, began trials with major food companies worldwide (though that catalyzed) instant social media backlash and conspiracy peddling, too. Link. Link. Link. Link.

• Beyond those energy and transportation-focused trends and statistics, the innovations and R&D I could speak to and try to curate here for you would quite literally be too many for me or probably even an advanced LLM to aggregate for you. While climate tech investment is falling across most types of fundraising and especially venture capital stages, I’ll keep highlighting the cool stuff coming to market here for you.

Top Keep Cool content from 2024

Based on some basic stats, these were the three most-read articles I wrote this year for Keep Cool. Let me know what your fav was (obviously including if not one of these).

& these were my favorite ones to write:

On the (still raging) debate around whether LNG is “better” than coal (an entirely pointless debate (in my opinion) once you factor in air pollution and coal mine methane emissions). Link.

On how (much) “greener” steel already exists (and it’s made in the U.S.A.). Link.

My pre-election take on why the election was never what mattered most to climate and energy-related things this year in the first place. Link.

A more philosophical post-election piece on clarifying what we’re actually trying to accomplish (whether with respect to climate tech and energy or otherwise). Link.

On geoengineering, which also got a lot more attention this year (as it should). Link.

On how climate tech companies are dying in droves, and that’s OK, even welcome. Link.

On how the future of our climate change trajectory is all on China and India. Link.

On the death of a specific climate tech business and how that’s, again, OK. Link.

On what sustainability really means (hint—it’s not just about emissions). Link.

On biodiversity, an oft-overlooked topic in climate and energy circles. Link.

More exceptional content from elsewhere

I released myself from feeling obligated to pen a longwinded narrative summary of all that transpired in climate tech, energy, and all other related topics this year (given those topics intersect with everything that happens on Earth). So here’s some other great content to check out if you find yourself with the capacity and curiosity for more reading soon.

• Climate Compass – a report on “some of the most influential themes, founders, and companies working toward climate resilience and global decarbonization.”

This report, produced by a veritable “who’s who” of standout individuals and organizations across the field, is well worth a read as it basically does a better and more comprehensive job of things I attempt to accomplish in these pages. In the words of Lily Bernicker, a Partner at Wireframe Ventures, it “maps critical themes across mitigation, adaptation, and removal and covers the next-generation of leading climate startups within each of them.” Get your hands on it fo' free here.

• Decarbonizing the power sector while demand grows – There’s another excellent new report out from an inimitable group of leaders titled “Fast, scalable, clean, and cheap enough: How off-grid solar microgrids can power the AI race, debates raged about the intricacies of the report and the fact that it outlines the need for backup power generation from natural gas for, say, for 5-10% of the time.

It sparked a brouhaha on Energy Twitter (apparently, and across all “aisles” of the spectrum) that I was luckily not really around for as it probably saved me some stress and in some cases, brain cells. Newsflash: Global emissions are still making all-time highs every year. Natural gas isn’t going anywhere for a long time.

Check out the report if powering data centers and getting real about decarbonizing alongside load growth is something you’re actually interested in with an open mind and genuine intellectual curiosity. Read it here.

• Massachusetts Climatetech Studio – Are you ready to share your passion, expertise, and vision for climate change but haven't figured out how yet? 2025 is your year.

The Massachusetts Climatetech Studio matches individuals and teams of entrepreneurs with cutting-edge tech from federal and university labs, plus resources to get work out of the lab and into the field.

The studio is launching its next 16-week cohort in 2025, and they'd love to have you onboard if you're an aspiring or experienced entrepreneur and if what's laid out above speaks to you. You DO NOT need to have your idea or technology—the studio and cohort program is designed to help teams license innovative IP and transform it from lab-stage to startup mode.

The program is primarily virtual and flexible for those working full-time. Massachusetts residents are encouraged; ALL are welcome. Each participant receives a $15,000 stipend, plus the opportunity for further prizes & grants (nor do you ever give up any potential equity in a business you may launch).

Applications are due Feb 28. Explore more FAQs, upcoming info sessions, and apply here.

• Invebitable, Obvious – My good friend Paul Gambill also has a new substack with a brilliant title (“Inevitable, Obvious”) that’s well worth subscribing to here.

25+ headlines

The good

• Commonwealth Fusion Systems, based out of Devens, MA, announced this week that it aims to build a grid-connected 400-megawatt (MW) commercial fusion power plant in Chesterfield County, Virginia. The company is targeting the early 2030s to energize the plant, with construction not expected until the “late 2020s,” given the time required to secure necessary permits are in place. Commonwealth Fusion Systems’s approach to commercial fusion focuses on magnetic confinement fusion using superconducting magnets to confine fusion reactions. The company raised a $1.8 billion Series B in 2021, making it the best-funded private sector company in the world. Link. Link. Link.

On the nuclear fission front, state-owned French utility EDF connected the first new nuclear reactor to France’s grid in 25 years. The Flamanville-3 reactor offers 1.6 gigawatts (GW) of output, raising France overall atomic capacity to about 63 GW. France is the world’s leader in terms of nuclear fission’s share in its power grid mix. Link.

• The EPA, the Supreme Court, and the Biden administration all OK’d California to proceed with its vehicle emissions limit policies and ban sales of new gas cars by 2035. Almost a dozen other states, plus leading automakers, have also adopted California’s strict vehicle emission standards, so these decisions could well propagate. That said, Trump’s administration will likely try to kill it all somehow still, and it may well devolve into a litany of long court battles. Link. Link. Link. Link. Link. Link.

• Chinese developers connected one of the world’s largest solar projects to the grid this week. Coming in hot at 4 gigawatts (GW), the project is located in the southeastern edge of the Taklamakan Desert. For context, that’s more solar than there is in all of Canada. Link.

• The DOE and its Loans Program Office were also immensely and incredibly busy this week (allocating more than $35 billion across closed and conditional loans) as it’s time to allocate federal funding for climate tech and energy infrastructure prior to the Trump administration taking things over draws nigh. While this last push to get funding across the line is welcome, it’s fair to question whether all parties involved here moved too slowly, as invariably, there’ll be unallocated funds and loans that, while granted conditionally, won’t close.

Here’s all that was announced, at least as far as I could aggregate it:

PG&E was awarded a record $15 billion conditional loan commitment from the Loan Programs Office to expand hydro and battery energy storage projects, upgrade grid infrastructure and grid-enhancing technologies, and aggregate virtual power plants. All parties involved will work to close the loan before the Trump administration takes over on Jan. 20. This marks one of the largest ever such loan commitments. However, it’s fair to ask whether one of the largest utilities in the country is the best recipient of it, given the LPOs’ overarching prerogative to fund projects that might not happen otherwise. Link. Link. Link.

The DOE also finalized a $9.6 billion loan to help Ford and Korea's SK On joint venture, BlueOval SK, build up to three factories in Tennessee and Kentucky to produce batteries for Ford EVs. The factories could add 120 GWh hours of annual U.S. battery production capacity. Link. Link. Link. Link.

The LPO closed a $7.54 billion loan to StarPlus Energy to finance up to two lithium-ion battery cell and module manufacturing plants in Indiana. The factories will make batteries for a joint venture between Stellantis and Samsung SDI to make EVs in North America. Link.

The LPO announced a conditional loan guarantee of up to $2.5 billion for Wisconsin Electric Power Co. to deploy more than 1,650 megawatts of utility-scale projects in wind, solar, energy storage, and hydropower. Link.

The LPO closed a $1.45 billion loan guarantee to Hanwha Q Cells to build facilities in Cartersville, Georgia, to make ingots, wafers, cells, and finished solar panels. When finished, the plant will be the largest ingot and wafer plant ever built in the United States. Link.

The LPO closed a $1.25 billion loan for EVgo to install 7,500 public EV chargers, including 350kW DC fast chargers capable of charging two cars simultaneously, at 1,100 stations nationwide. Link.

The LPO offered Novonix, a battery materials company, a conditional commitment for a direct loan of up to $754.8 million from the DOE's Loan Programs Office to build a new synthetic graphite manufacturing plant in Tennessee. Link.

The LPO announced a conditional commitment of up to $559.4 million for subsidiaries of Convergent Energy and Power to one solar + storage and three stand-alone storage projects in Puerto Rico. Link. Link.

Technip Energies, a French energy engineering company, and LanzaTech, a carbon recycling company based out of Skokie, Illinois, announced the DOE’s Office of Clean Energy Demonstrations committed up to $200 million for a Sustainable Ethylene from CO2 project the two companies are developing in tandem. Link.

Toyota will receive $4.5 million in DOE funding from ARPA-E to develop infrastructure and technology to make more circular, automated EV battery supply chains. Link. Link.

• Oklo, a Santa Clara, California-based developer of advanced small modular nuclear reactors, announced it signed an agreement to sell 12 GW of power from new nuclear projects to Switch, a data center development company, with an unclear start date—ASAP, presumably—through 2044. While the agreement is non-binding, it's one of the largest deals of this type for lower-emission energy ever, adds to the story we’ve been tracking surrounding data center energy demand growth and how it’s impacting the energy transition, and highlights the insatiable need for more low-emission electricity in general. I love a good announcement, but I will bide my unbridled optimism until one company actually builds one working advanced nuclear fission or fusion plant, even a demo. Link.

• NuVision Solar, a U.S.-based solar manufacturer, came out of stealth this week and announced it will build a solar cell and module assembly plant in the U.S. It’s targeting a 2.5 GW capacity and to begin module production in Q4 2025 for utility-scale, large-scale commercial and residential solar markets. Link.

• Avina Clean Hydrogen announced it will build a new aviation fuel (SFA) factory in Illinois with state-level funding. Link.

• Sometimes you don’t get denied: After significant pushback, Doral Renewables received approval to develop its 1.3 GW solar project, “Vista Sands,” in Wisconsin. Link.

• Einride initiated commercial daily operations of fully autonomous trucking in Morgongåva, Sweden, marking Europe's first commercial autonomous daily trucking operations. Link.

• EV battery beast CATL announced it will get into battery swapping in China and plans to open 1,000 stations next year. Battery swapping is already a ‘real’ thing in China, and U.S. companies are trying, too. Link.

• Lithium-sulfur battery startup Lyten secured a $650M LOI from the Export-Import Bank of the United States to expand its graphene manufacturing footprint (for batteries) in the U.S. Lyten is taking over Northvolt's Cuberg factory in San Leandro, CA, and plans to build another factory in Nevada. I’m not always bullish on LOIs alone, as 2024 was a year in which many grand plans and announcements (as always) were also scaled back or scrapped. Ideally, this thing gets built. Link.

• Fortera, a lower-carbon cement manufacturer, announced a partnership with Sumitomo Corporation to deploy Fortera’s cement plants with large Asian cement manufacturers. It’s just a Memorandum of Understanding (MOU) so far, but still cool. Link.

The inbetweens

• Chinese battery giant CATL is considering (for the second time) whether to list on public market exchanges in Hong Kong. It could raise $5 billion or more in the process. Link.

• Vistra, an integrated power company, announced two new utility-scale solar projects in Illinois connected to the grid. That said, it also noted it will have to delay retiring a 1.12 GW coal power plant in Baldwin, Illinois, from 2025 to 2027 (for now, could well end up being longer. Link.

• Chinese battery exports jumped to $1.9 billion last month, as exports to the U.S. hit a record high in November to get products out the door before the next U.S. government may remove tax benefits. Link.

• Honda and Nissan, the 8th and 9th largest automakers globally. are reportedly discussing a merger to better compete with intensifying competition from China and Tesla. Link. Link. Link.

• The outgoing Biden administration raised decarbonization goals, ratching them up to target U.S. greenhouse gas emissions reductions to a drop of at least 61% below 2005 levels by 2035. The previous goal was 50-52%. Regardless of who does what, these goals will not, unfortunately, be met. I can promise you that, as the current progress is about ~20%, 2035 is now ten years away. Link.

• A lengthy new analysis on the U.S. LNG market is out, covering everything from LNG’s climate impacts to energy markets, geopolitics, and more. The wonks are arguing about it. I’m not going to get into it—LNG is better for the world than coal, full stop. You can read more in the links; it’s not like the next administration will necessarily make different decisions on approving LNG export terminals, regardless of the report’s initial conclusions. Link. Link. Link. Link.

The bad

• King coal: In November, China logged new above-ground coal mining records, mining more than 428 million tons of what is still the world’s number one fossil fuel. Two things can be true at once: China adds more renewable energy and other low-carbon infrastructure (and does so much more quickly than anyone else), and it still consumes and produces more than half the world’s coal. While coal consumption is falling in the U.S. and Europe, it is rising in the rest of the world, especially in India and other Asian countries, like Indonesia, as we have covered extensively. Coal is still the number one fuel for primary energy globally, and the world may not hit peak coal until 2027 or beyond. Link. Link. Link. Link. Link. Link. Link.

• Given the above, among many other drivers, 2024 global warming will likely breach the 1.5°C mark. Link.

• Shocker: Federal permitting reform to accelerate energy infrastructure in the U.S. did not come to pass this year, as a bipartisan Senate bill that had shown some signs of life didn't make the final year-end spending deal. This bait and switch happened a few times this year (*sighs audibly*).

• On that note, oddly enough, maybe the incoming Trump administration will be the one to do advance permitting reform, though it could well end up being much more favorable to fossil fuel-focused infrastructure. Link. Link.

• Weather is getting so weird existing weather models aren’t working anymore. Link. (paywall).

• Walmart, the world’s largest retailer, does not expect to meet its 2025 or 2030 emissions targets. The company previously pledged to cut its emissions by 35% by next year and 65% by the end of the decade. Emissions in 2023 were up 4% year-over-year. Link.

• BlackRock wrote down the value of its ‘Global Renewable Power Fund III’ after several of its investments, like Northvolt, failed. Performance was at <0% IRR by Q3 2024. Link.

• Getting rejected is always tough: In Austria this week, multiple Austrian states released new zoning plans that will effectively kill large wind farm projects. One 500 MW project was already under construction. Elsewhere, a local council in Victoria, Australia, blocked a 500-MW solar + storage project (500 MW solar + 300 MW BESS) on fears “it would harm the local environment,” as if continued greenhouse gas emissions won’t. Link. Link.

• Two Russian oil tankers were damaged in inclement weather near the Black Sea, spilling and leaking thousands of tons of oil. Link.

• Tesla appears to be experiencing significant quality control issues with self-driving computers in new vehicles. Link.

• Comparable to news that we covered last week about Nikola approaching bankruptcy, Canoo, a U.S. EV startup manufacturing that hasn’t made nearly as much progress as others like Rivian and even Lucent, also appears to be on its last leg and initiated more layoffs. Link.

CURATED DEALS

Larger funding rounds

⚡ Fervo Energy, based out of Houston, raised $255 million across growth equity and debt funding for its enhanced geothermal energy development business. California State Teachers Retirement System (CalSTRS), CPP Investments, Congruent Ventures, and others invested. Fervo has been one of the year’s allstar climate tech and lower-emission energy companies, by a country mile, delivering stellar performance results on projects it’s actively developing versus future promises alone. Link.

🏠 1KOMMA5, based out of Hamburg, raised ~$156.6 million in pre-IPO Financing to provide solar, energy storage, EV charging, and heat pumps to homeowners. G2 Venture Partners and California State Teachers’ Retirement System (CalSTRS) led. Link.

⚡ CleanCapital, based out of New York, raised $145 million in equity funding to invest in and operate solar and energy storage projects in business settings as well as for schools, municipalities, and more. Manulife Investment Management invested. Link.

Medium-sized funding rounds

🔌 Jet Charge, based out of Melbourne, raised ~$45 million in equity funding for its EV charging company that operates a “charging as a service model.” Mirova led. Link.

🔋 Nanoramic, based out of Wakefield, MA, raised $44 million in equity funding (I presume) to make battery materials. General Motors Ventures and Catalus Capital co-led. Link.

🔋 Bnewable, based in Brussels, raised ~$44 million in equity funding to develop battery and energy management systems for businesses. RGreen Invest led the round. Link.

🏭 Haber, based out of Pune, India, raised $38 million in Series C funding to develop AI-powered automation services for manufacturers to improve efficiency and mitigate environmental externalities, primarily by focusing on water use but also on energy use. Creaegis, Beenext, and Accel invested. The company also raised $6 million in debt. Link.

🤖 It’s all robots these days! Slip Robotics, based out of Atlanta, raised $28 million in Series B funding to scale up the production of robots to help accelerate truck-loading and reduce the time trucks spend idling at warehouses, which reduces emissions. DCVC led. Link.

🔌 Boon, based out of San Francisco, raised $20.5 million in Series A funding to make AI tools to help automate fleet management operations. Marathon and Redpoint Ventures led. Link.

✈️ Vaeridion, based out of Munich, Germany, raised $14.7 million in Series A funding to make technologies for electric aviation. World Fund led. Link.

♻️ Hauler Hero, based out of San Diego, raised $10 million in seed funding for its cloud-based software platform that helps automate operations for waste management companies. I2BF Global Ventures led. Link.

Smaller funding rounds

🧊 Mojave Energy Systems, based out of Sunnyvale, CA, raised $9.5 million in Series A funding to make more energy-efficient commercial air conditioning systems that use liquid desiccant technology. Fifth Wall and At One Ventures led. Link.

🚌 Zingbus, based out of Gurgaon, India, raised $9 million in Series A funding to build a network of electric intercity buses. BP Ventures led. Link.

🗑️ Orbisk, based out of Utrecht, Netherlands, raised $8.4 million in Series A funding for its food waste monitoring software to reduce food waste in hospitality. Regeneration.VC and PeakBridge co-led. Link.

🌾 hemav, based out of Barcelona, raised $8.4 million in equity funding for its agricultural platform ‘LAYERS’ that aims to reduce input costs and deliver better yield predictions. Future Food Fund, PureTerra Ventures, and Inclimo invested. Link.

👷 SmartAC.com, based out of Houston, raised $8 million in extended Series B funding for its platform that uses sensors and software to help contractors monitor HVAC systems. Mercury Fund led. Link.

🔧 Cadstrom, based out of Montréal, raised $6.8 million in seed funding to make AI tools that help electrical engineers detect errors and validate complex electronic hardware designs. Bison Ventures led. Link.

📊 Sunairio, based in Baltimore, raised $6.2 million in equity funding for its AI-driven weather and climate modeling software. The software uses high-resolution climate simulations to help energy companies predict weather patterns and market changes. Buoyant Ventures led the round. Link.

🌬️ Triton Anchor, based out of Chelmsford, MA, raised $2.2 million in seed funding to make anchors for offshore wind farms. MWNW Consulting Group and a Scottish family office co-led. The company was also selected for $3.5M in new non-dilutive grant funding. Link.

🧊 Conry Tech, based out of Melbourne, Australia, raised $1.6 million in pre-seed funding to make more efficient modular air-conditioning units for commercial buildings and data centers. Bandera Capital led. Link.

🔎 Artem, based out of Cham, Germany, raised $1.6 million in equity funding for its combined software and hardware platform to help companies navigate CBAM compliance. Vireo Ventures led. Link.

Other funding rounds

⚡ Repsol, based out of Madrid, raised ~$362 million in debt financing to build 400 MW of wind and solar energy projects across Spain from banks like Credit Agricole. Link.

⬇️ Frontier, the advanced market commitment group for carbon removal, facilitated $80 million in offtake agreements for two carbon removal companies, namely CO280, which develops Biomass Carbon Removal and Storage (BECCS) projects, and CREW, which removes CO₂ from wastewater treatment processes. The deals depend on the delivery of 224,500 tons of CO₂ removal from CO280 between 2028 and 2030 and 71,878 tons of CO₂ between 2025 and 2030 from CREW. Link.

🧪 Verde Clean Fuels, based out of Houston, raised $50 million from Cottonmouth Ventures to build natural gas-to-gasoline production plants. Link.

🔋 Nouveau Monde Graphite, based out of Saint-Michel-des-Saints, Canada, raised $50 million in equity funding to make graphite for batteries from the Canada Growth Fund and the Government of Québec. Link.

🔋 Form Energy, based out of Somerville, MA, raised $50 million in equipment financing from Trinity Capital for its iron-air energy storage systems. Link.

⛏️ Patriot Battery Materials, based out of Vancouver, Canada, raised $48 million in equity funding for its lithium production business from Volkswagen, which took control of about 10% of the company. This marks VW’s first direct investment downstream in the lithium supply chain. Link.

⬇️ Deep Sky, based out of Montreal, Canada, raised $40 million in grant funding from Breakthrough Energy Catalyst for it to build its ‘Deep Sky Alpha’ project in Alberta, where it will develop, test, and deploy direct air capture technologies. Link.

♻️ Yeastup, based out of Brugg, Switzerland, raised ~$9.9 million in Series A funding to repurpose a dairy factory to upcycle 2,000 tonnes of spent brewer’s yeast annually into proteins and other ingredients for food, nutraceuticals, and cosmetics. Beyond Impact, Gentian Investments, Newtree Impact, and Angel House invested. Link.

🔬 Greentown Labs, based out of Somerville, MA, raised $4 million in funding (I’m not sure exactly what type of funding tbh) for its climate tech incubator, which is North America's largest. Rice University, MassDevelopment, and others participated. Link.

⚡ Pattern Energy, based out of San Francisco, raised an undisclosed amount of equity funding to develop wind, solar, transmission, and energy storage projects globally. Investors included APG Asset Management and Australian Retirement Trust. Link.

🌬️ Apex Clean Energy, based out of Charlottesville, VA, raised an undisclosed amount in tax equity financing to build a 300 MW wind project in Piatt County, Illinois (the project is already under construction). JP Morgan led the tax equity commitments. Link.

🏗️ Buildforce, based out of Houston, a startup that connects skilled tradespeople like electricians with construction contractors, acquired Ladder, an Atlanta-based startup backed by Y Combinator that builds a technology-enabled construction labor marketplace to (also) connect skilled tradespeople (like construction workers) with contractors. Terms and transaction details were not disclosed. Link.

New funds

💵 TPG, based out of San Francisco, raised commitments totaling close to $2 billion for a new climate-focused private equity infrastructure fund. Link.

💰 Category Ventures, a new VC based in San Francisco, launched and raised $160 million for its first fund. It will make $1.5 million to $5 million in pre-seed and seed investments in startups targeting AI, infrastructure, developer tools, and more. I reckon some of those AI and infrastructure investments will flow to energy and energy efficiency applications. Link.

💰 Heartcore Capital, based out of Copenhagen, raised $180 million for its ‘Fund V,’ out of which it will invest in 25-30 startups across areas including synthetic biology, AI, and climate tech. Link.

Sorry for writing this many words this year. Next year, I’ll aim for ¼ as many. Truly.

Enjoy the glowing embers of 2024. Here’s a pic from Joshua Tree with friends.

– Nick

Reply