- Keep Cool

- Posts

- 2023 year in review

2023 year in review

Nick van Osdol

December 21, 2023

Hi good people,

Another one bites the dust. Another year in the books, that is. I want to extend a warm thank you to you for being here. The size of this audience is much larger now than I could have imagined a year or two ago. It’s four times the size of the town my grandma lives in. It gives me twice weekly ‘Torschlusspanik’ to think of what to say to y’all (a fun problem to have).

For today, I’ll aim to offer a digestible 2023 ‘year in review’ with respect to where climate and energy meet business. Digestible won’t mean it’s short; you know me by now. Pictures help.

The newsletter in 40 words: The world is both doing a lot and simultaneously, not nearly enough to respond to cascading climate challenges. This newsletter explores both the bright spots in 2023, calls to action, as well as a sober treatment of the challenges ahead.

DEEP DIVE

Before we begin, let’s get on the same page about one thing, namely that collectively, we are doing a lot and also not doing enough. Open yourself up to the fact that these can simultaneously be true.

Sitting at the cusp of 2024, from my vantage point, I see an immense amount of ‘energy’ pouring into climate tech and energy transition work across the public and private sectors, from the level of international politics to grassroots and individual activism. This is great. This wasn’t nearly as true ten years ago. At the same time, as noted by PwC’s research team in Q3:

The global rate of decarbonisation remains far too slow: recent PwC research finds that the world needs to decarbonise seven times as fast as the current rate to limit warming to 1.5°C above pre-industrial averages.

If we can together hold these things to both be true, then we can pass go and proceed.

At the highest level…

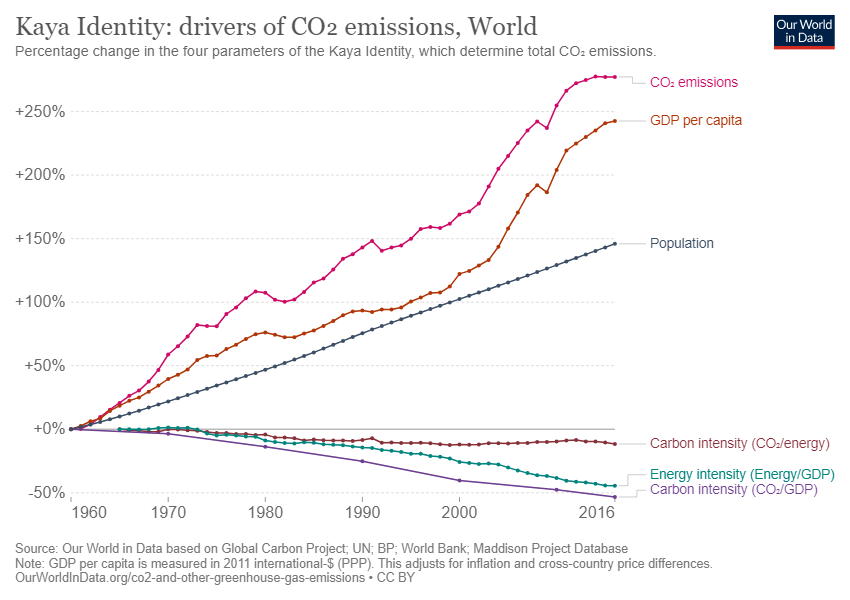

At the highest level, the main thing you should know about the state of climate tech, as it were, is that global emissions of most major greenhouse gas emissions – carbon dioxide, methane, and nitrous oxide rose – again in 2023. Even as in places like the U.S., renewable energy closes in on logging new milestones, such as overtaking coal-fired electricity generation, globally, coal production, consumption, & seaborne volumes all still hit all-time highs in 2023.

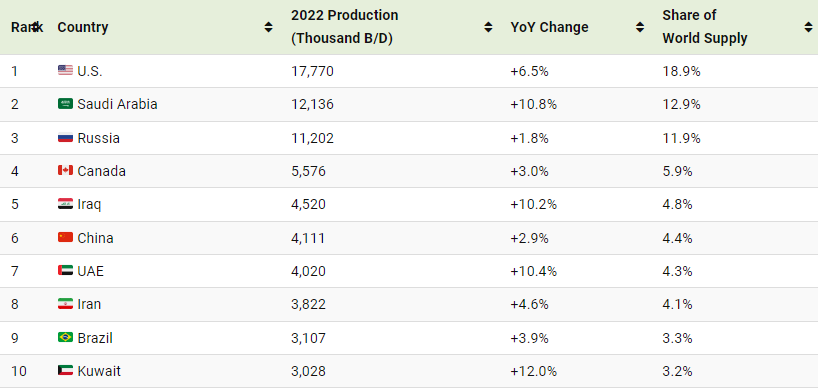

Similarly, and even under a progressive, climate-focused administration, U.S. oil production will chart new records this year. It will probably do so in 2024, too. As much as we like to point fingers at China for, say, their coal consumption, well, the U.S. is the world’s largest oil producer! By a wide margin.

Don’t worry; this newsletter isn’t intended to discourage you. But, as much as my work here often lilts towards optimism, it’s also my job to offer a sober perspective. The enchantment and excitement that have swirled surrounding climate tech, renewable energy, EVs, and whatever else in 2023 has been awesome. It is important that I, that we, ‘sell’ climate tech as a success story, as sexy, to those on the outside looking in or to folks who are as-of-yet skeptical. But we shouldn’t get too self-congratulatory. As some of my favorite newsletter writers over at Blackbird Spyplane wrote this week, sometimes, “blowing up bulls**t with panache goes hard!!”

What’s my point? At the highest levels, climate challenges are still getting worse. Not better. Commitments from major emitters aren’t translating to progress quickly. I say this not to discredit any company, policymaker, or individual’s efforts or work. We’re gathered here to make progress. I say it because I feel like I have to; ‘cuz I don’t see it articulated clearly elsewhere often, to be honest.

Something that’s also less discussed is that a lot of this has to do with population growth. Which isn’t going anywhere. Yes, the intensity of emissions per unit of energy production globally has and is going down. Slightly. Which is good! But what hasn’t and what won’t change is the growth in energy demand in general as the world’s population grows.

We are trying to turn around a massive, proverbial oil tanker with a full head of steam in choppy seas. It’s vital we try. But no one said it was going to be easy.

On the funding side

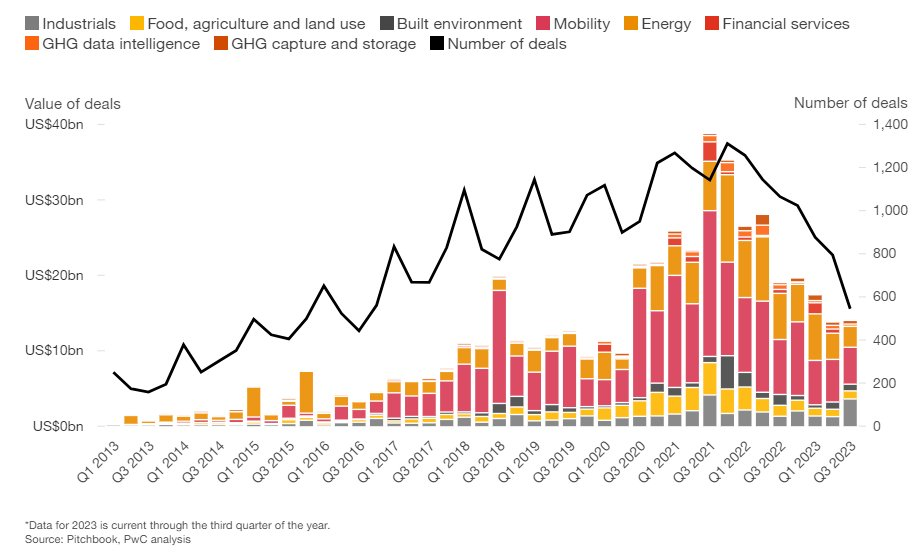

Climate tech venture funding has taken a step back from 2022 and 2021 to 2023. This is most visible in things like the raw number of deals getting done (data and visualizations from PwC) below but is also true for things like total fundraising across most stages and sectors.

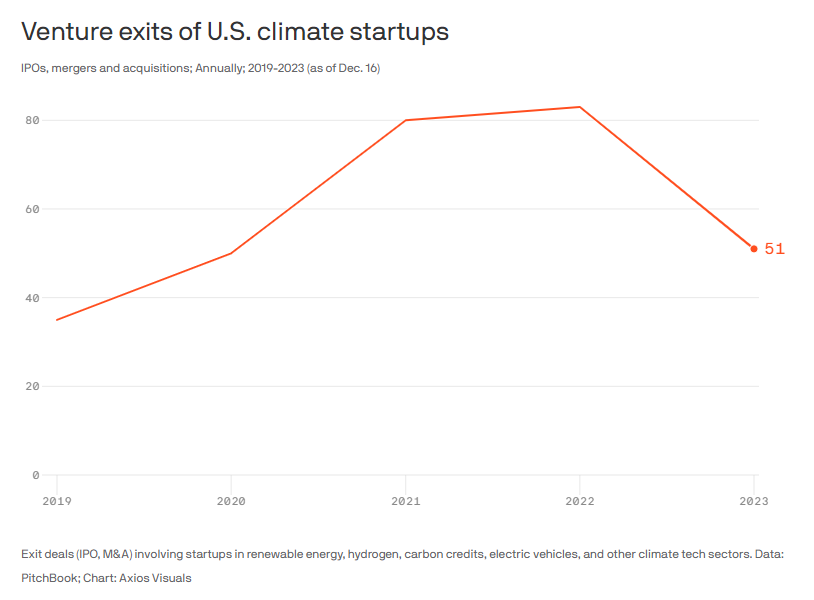

Exits for venture investors were down, too, which isn’t great either. Exists are what venture investors need to stay committed to investing in any sector or tech trend. Absent opportunities to realize returns, appetite to fund deals wanes.

On a brighter note, climate deals did claim a growing share of total venture investment. What this effectively means is that while climate venture funding saw a downturn, that was driven by a broad-market venture slow-down. Climate’s share of venture funding overall rose.

Some sectors also bucked the general down-trend in venture investment. Carbon removal was a noteworthy stand-out. That’s also a bit weird, though, considering that’s a 1% solution as opposed to, you know, reducing emissions. Often and unfortunately, venture allocations trend a bit askew.

What do I make of the slowdown in venture funding for climate tech? Honestly, I think it’s OK. If we imagine for a moment that climate and energy transition work is a big house, venture capital is never going to be a load-bearing wall. Most of what needs to happen to make meaningful progress in addressing climate change is serious infrastructure deployment and wholesale changes to how we produce energy, move ourselves and goods around, farm, and live. That type of change typically requires a whole ‘nother category of finance.

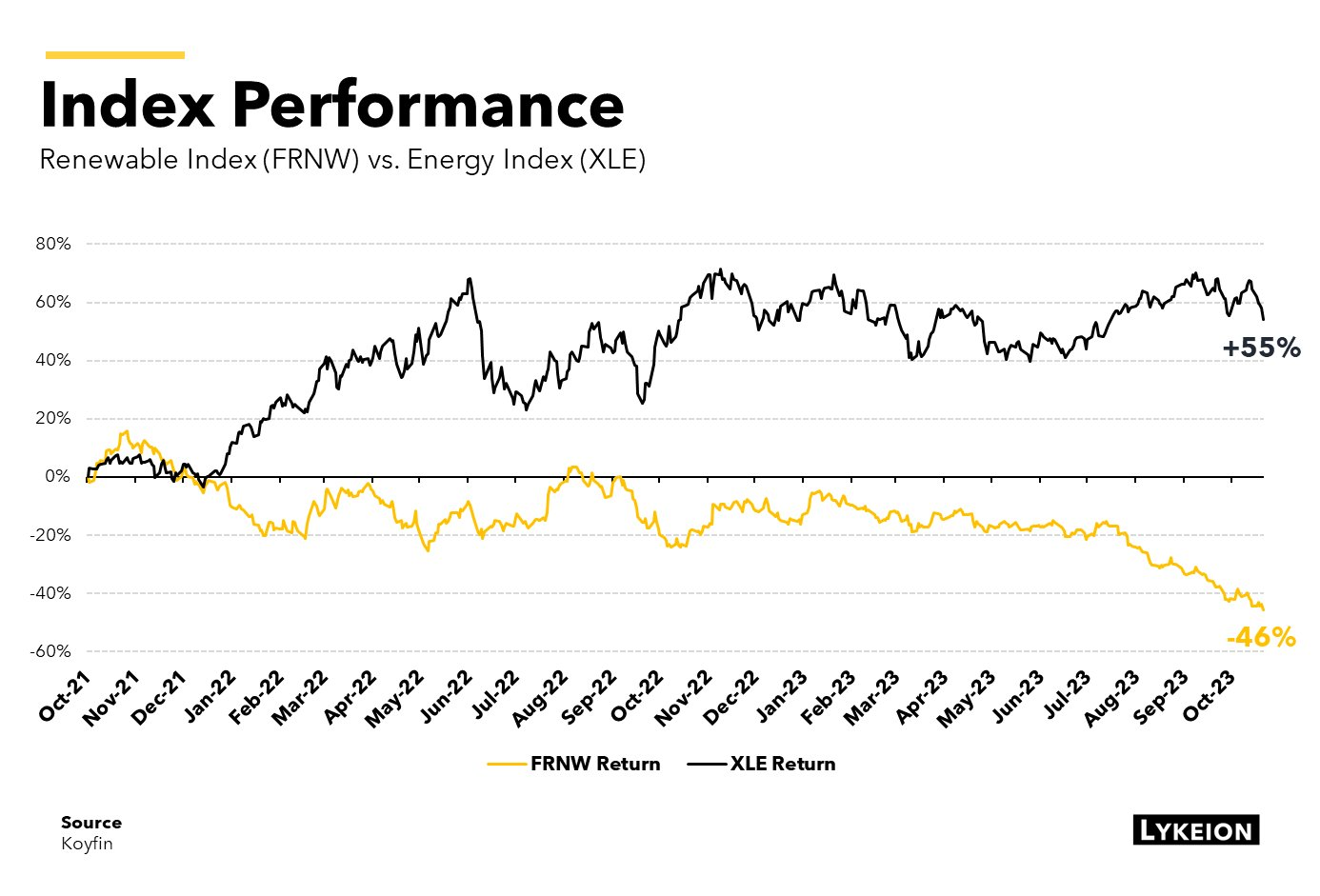

In terms of said other categories of finance, some of those took steps back, too. As interest rates rose globally, capital-intensive project deployment faltered. Wind energy is a good example; the industry got hammered this year. Renewable energy development, in general, took a big hit.

This is, again, neither here nor there for me. Interest rates are going to ~ interest rate ~. Many lament the rise in interest rates and the negative short-term impacts higher rates have wrought on infrastructure deployment. I’d offer that, at the same time, interest rates are an essential hurdle rate for productivity. It’s not like we collectively moved money to its highest and best uses when interest rates were 0% in 2020 (*cough cough*, crypto / 15-minute grocery delivery / electric scooter apps).

Where does that leave us? In 2021 and much of 2022, climate tech was 'up only.' Now we're in a phase of the market cycle where, almost every week, a once buzzy climate tech company is either announcing layoffs or going out of business entirely. Here are examples from Q4 alone:

Solar: Sunfolding, a solar startup with a novel pneumatic tracker solution, went out of business this month. It had raised $30M+ in venture funding.

Energy storage: Zinc8 Energy Solutions, based in Vancouver, has cut all non-essential staff. The CEO also resigned as the company explores asset sales. The company previously raised $20M+ in venture funding.

Transportation: Volta Trucks, a Swedish EV truck manufacturer, filed for bankruptcy. The company has raised more than $390M, including a $300M+ Series C last year.

Built Environment: Veev, a modular construction technology company that raised ~$600M, is purportedly close to going out of business.

Food & Agriculture: Fifth Season, a U.S.-based robotic vertical farm startup, filed for bankruptcy and liquidation. It had previously raised $35M in venture funding.

E-mobility: Bird Scooter (finally) filed for bankruptcy. The company raised $883M and was once valued as high as $2.5B.

Markets cycle. Anyone who sold you on a story that this wouldn't happen to climate tech because of the necessity of climate action was not an honest broker. Sorry. Markets (and everything else in this life) need waves of creative destruction. Capital that flowed to less-than-optimal solutions gets chewed up. But spring follows winter. Hopefully, we learn.

To close this section on a brighter note, a lot of non-venture institutional capital was allocated to climate this year. It hasn't been deployed yet for the most part; there's a veritable war chest waiting to fund solutions for the rest of the decade. Hopefully, it does get allocated over the next 5-10 years; that isn't guaranteed. Still, the fact that preeminent private equity and banking names ranging from Blackrock to Goldman Sachs to KKR got in on the act is a positive:

For one, there's the new $30B fund the UAE announced at COP 28 that it is building with Brookfield, Blackrock, and TPG.

Blackstone raised $7.1B for a 'Green Private Credit Fund,' one of the largest private credit energy transition funds ever.

Apollo formed a new entity, the Apollo Clean Transition Capital, with $4B to pursue "an investment strategy that intends to redefine the capital market for climate solutions."

KKR raised $2.8B for its second global impact fund.

Brookfield Asset Management and Societe Generale co-launched a new private debt fund with €2.5B of capital to invest in power, transportation, and other projects.

Copenhagen Infrastructure Partners raised $2.1B across two new energy funds.

Paine Schwartz raised $1.7B for a food and ag-focused private equity fund.

Goldman Sachs raised $1.6B for its first private equity vehicle to focus on climate.

Those eight sample bullets alone represent more than $50B in capital. Here's to hoping it moves!

Manufacturing and commercialization

Building back towards a more upbeat tone, there was a lot of investment in commercial manufacturing capacity in 2023. That’s probably one of the standout stories from both last year and this year. This is especially true domestically, where incentives from the IRA and CHIPS Act have unleashed a wave of domestic manufacturing commitments. The IRA established a tax credit of $35 per kilowatt hour for domestically produced battery cells, covering roughly 20-30% of typical battery costs. This, as well as other new policy requirements and incentives, have made domestic manufacturing more attractive again. It’s genuinely a bit of a miracle; most wrote American manufacturing off for dead a long time ago.

Practically speaking, this miracle looks like companies ranging from Toyota to Hyundai to First Solar and Tesla investing billions of dollars to build manufacturing facilities in the U.S. to make batteries, solar panels, and more. Some of this is happening in Europe, too; Northvolt has raised billions of dollars & secured more than $50B in customer contracts to establish a lithium-ion battery supply chain in Europe. It’s currently building three gigafactories across Europe in northern Sweden, Germany, & Poland. Between the 3, it aims to have more than 170 GWh in annual battery production capacity. It’s also building a gigafactory in Canada.

Suffice it to say there were many factory announcements in the U.S. this year. More than $250B has been allocated to new factories in the U.S. alone since the passing of the IRA and the CHIPS Act. Here are some of the biggest announcements to date:

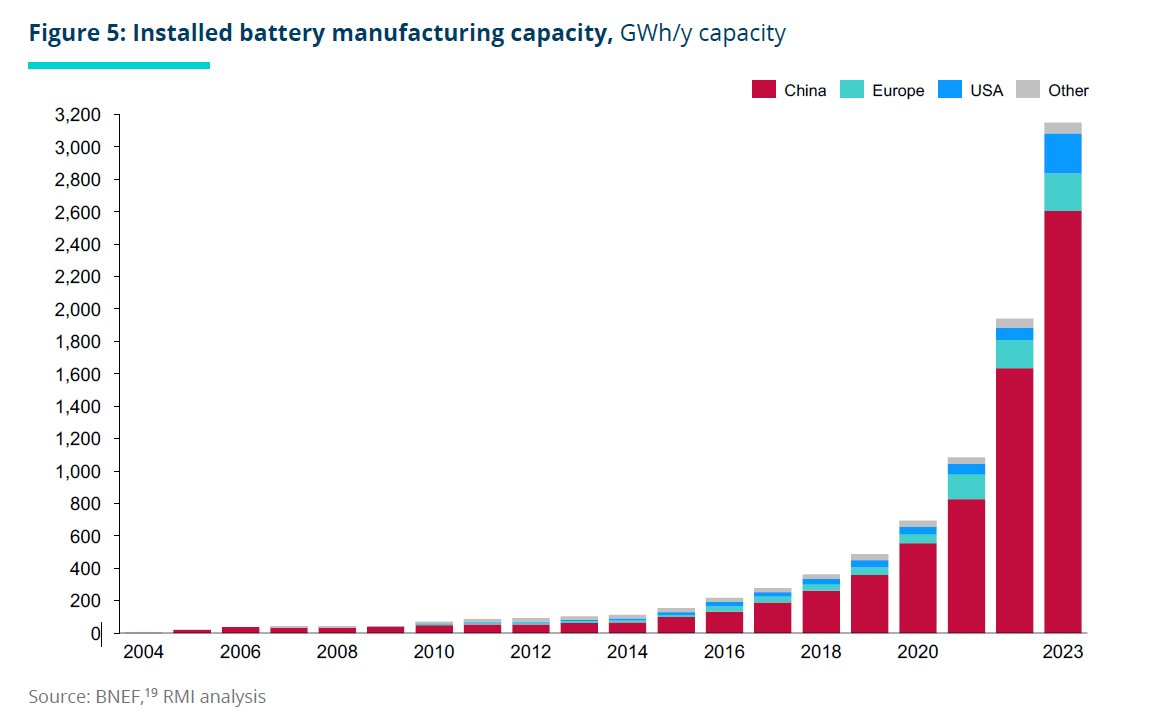

Another thrust of this investment in Western manufacturing capacity is encapsulated in the graphic below. It depicts installed battery manufacturing globally. Most of the capacity is in China. That’s a problem, perhaps; European and North American countries don’t want to be wholly dependent on China to source technologies like renewable energy and EVs that are being deployed at exponential rates. While the chart depicts battery manufacturing capacity, it could just as easily represent solar panel manufacturing. Or lithium refining. Or copper production. A similar picture would hold.

Beyond the technology, investment, and capacity-building, one noteworthy callout is that most new factories are being built in red or at least purple (hotly contested) states. That makes manufacturing a powerful political lever. It's hard to resist the political allure of a new factory. Factories don't just come with jobs and economic revitalization. They're quintessential Americana; many parts of the country were built around heavy industry and manufacturing. That's important as we head into 2024, where, at least in the U.S., the Presidential election is one of the most critical climate stories (and stories in general). In many polls, Biden and Trump are neck and neck, or Trump has an edge.

To zoom back into the factories themselves, going forward, one of the things I'm most keen to watch over the next 5-10 years is how many of these factories begin operating on time, on budget, and at the nameplate capacities they touted when they were announced. Some of them are scheduled to start production at a serious scale as early as 2024. We'll see if that comes to fruition. Announcements don't equal finished factories. Nor do finished factories equal profits.

In the same vein, some or even many won't make it. Some announced projects, including ones that secured significant government funding, have already taken a hit. Take, for instance, Li-Cycle, which raised $375M in loan commitments from the DOE to expand a Rochester, NY-based battery recycling plant. The facility was targeting capacity to recycle batteries for 200k+ EVs annually. Construction is now on hold as Li-Cycle's future is uncertain.

Similarly, Panasonic noted this week that it's abandoning plans for a new Oklahoma battery factory. The company also has an EV battery factory under construction in Kansas, where it has come up close and personal with higher-than-expected costs. The Oklahoma plant was line item number 5 on the factory announcement graphic shared above, in case you needed proof that the gap between announcement and finished construction is, often quite wide.

OK… more good news please

I get it, this has been a bit downbeat so far. Here’s more of the good news.

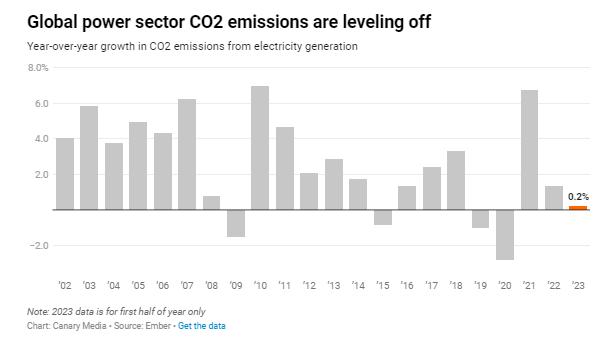

We may be close to peak power sector emissions globally. Again, that does not mean emissions are going down. It just means we may be close to a point where they stop growing. Still a cool milestone!

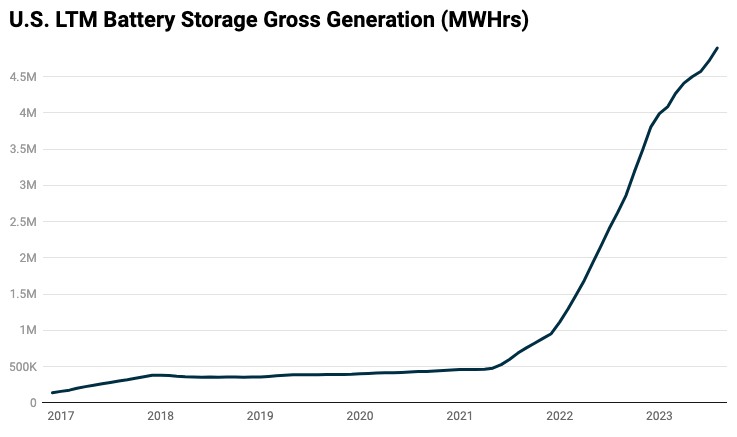

In the U.S., battery energy storage deployment and utilization took off. This is essential to make full use of renewable energy and to accelerate the next wave of their deployment. Wind & solar must be paired with supportive infrastructure, ranging from storage to transmission, to enable deeper decarbonization. Without storage, renewables are, at best, a fuel-saving technology; they offset natural gas or coal-fired electricity production. With storage, they can replace them entirely.

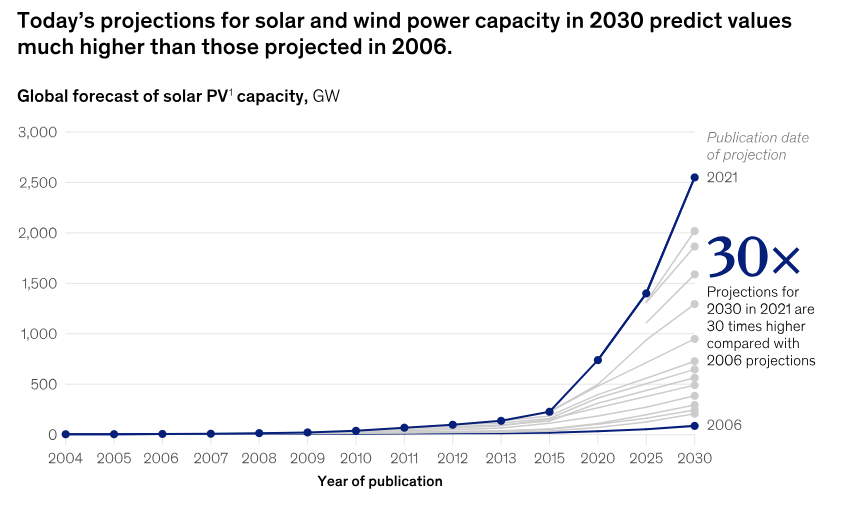

The things that give me the most hope are how routinely our predictions and expectations, including, for instance, how quickly China can continue to deploy low-carbon energy infrastructure, get smashed. China continues to make eye-watering progress in deploying renewable energy.

We are not good at predicting exponential growth. And thank god for it, given how current projections continue to suggest we’re not making nearly enough progress.

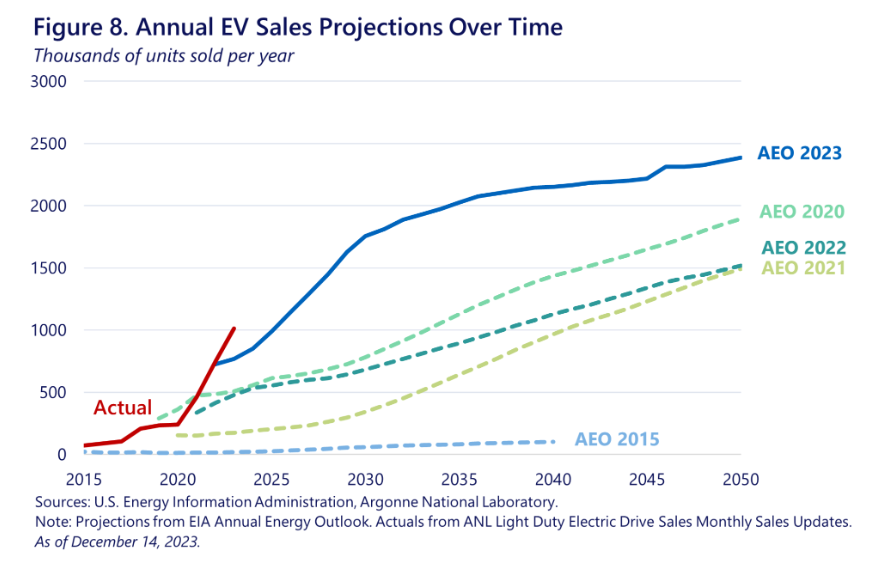

Another good example of this is the rate at which EVs are being adopted in places like the U.S. and Europe. Fully electric light-duty vehicle sales surpassed the 1 million milestone this year in the U.S. for the first time, representing more than 7% of light-duty vehicle sales in general. I don’t think anyone would have predicted that even three years ago.

Here's more good news, especially on the innovation front, in 11 notable bullets:

Fusion: Microsoft and Helion, a fusion-energy developer, inked a PPA for 50 MW of electricity. The PPA is for 2028, which would constitute a dramatically accelerated timeline for fusion deployment versus most analysts' expectations (including mine). Helion and Nucor, a steel manufacturer, also signed an agreement to develop a 500 MW fusion power plant co-located with a steelmaking facility by 2030.

Solar: Trina Solar started production on the world's first 700W solar panels.

Geothermal: America's first enhanced geothermal power plant, operated by Fervo Energy, produced low-carbon electricity and sent it to the grid for the first time in Nevada. The 3.5 MW project is supplying power directly to NV Energy, the local utility.

Energy storage: Northvolt, the burgeoning European battery manufacturing giant, announced a sodium-ion battery that it validated at 160 watt-hours per kg. The elements in the electrodes are all abundant (sodium, carbon, iron, and nitrogen).

Aviation: We saw the world's first trans-Atlantic flights to use 100% sustainable aviation fuel completed in a Gulfstream G600 aircraft and then, a week later, in a much larger airplane, a Boeing 787. ZeroAvia also made history by flying the largest aircraft ever to be powered by a hydrogen-electric engine.

Agriculture: Feed additives that reduce methane emissions from cows are progressing into major commercial trials on farms in the U.S. and the E.U. More on this in 2024.

Built Environment: Brimstone, a carbon-negative cement manufacturer, received third-party certification that its cement meets standards for portland cement, making it the first 'green' cement company to meet this industry requirement.

Steelmaking: Ohio-based Cleveland-Cliffs, an iron and steel manufacturer, has reduced greenhouse gas emissions by approximately one-third since 2017 by transitioning to direct reduction in its iron manufacturing.

Policy: The European Union and Canada both approved bans on new gas car sales by 2035, as did fourteen states in the U.S. This all started in California, evidencing how state-level policy can spread worldwide.

Policy / methane: The Global Methane Pledge gained steam: Countries representing 45% of global methane emissions have pledged to reduce methane emissions by 30% by 2030. I'll track actual progress here very keenly next year.

Conservation: Deforestation in the Brazilian Amazon fell significantly.

Time to open the aperture

You’ll note that much of what we’ve discussed so far has focused on the power sector and transportation. I did that intentionally to illustrate a challenge and offer an invitation. Climate practitioners, including myself, concentrate on these sectors disproportionately, even though they represent less than half of all contributions to global warming and even though global warming is only one of many climate challenges.

I basically embodied this power sector / transportation myopia for you for half a newsletter. Excuse my making this a piece of performance art, but hopefully, that drives the point home.

A recent meme of mine folks seemed to resonate with

Fortunately, many brilliant people are working to force the rest of us to ‘open our aperture.’

2023 was a good year for burgeoning focus on methane emissions, which stem more readily from agriculture than from the power sector and transportation (or even oil and gas on the whole).

2023 was a good year for burgeoning focus on biodiversity loss, a problem that’s driven by many factors, of which global warming is only one.

2023 was a good year for burgeoning focus on other pollutants, like microplastics, that have nothing to do with global warming at all and are insidious and ubiquitous.

Still, the power sector and transportation dominate. For instance, in 2020, one analysis found that globally, low-‘carbon’ transportation received 15x more investment than methane. Solar and wind energy received 26x more investment. Those figures have likely gone up in recent years as investments in electric cars and battery manufacturing (as discussed above), as well as renewable energy, have ballooned. Further, those figures compare specific solutions to all of methane, a category that includes emissions from many sources. Those numbers are ludicrous; by some estimates, methane has driven 30% of already observed global warming.

If this section is any indication, a lot of my work in 2024 will concentrate on trying to herald in the opening of the aperture I’m calling for here. Hopefully, my work in 2024 embodies what I’m trying to accomplish. I’m at least setting that intention now.

What else keeps me up at night?

Surprisingly, few of the things I noted as negatives in this newsletter so far. Nor is what keeps me up at night how much we know about climate science or how slow progress on addressing climate change is. It's how much climate scientists don't know about what havoc climate change will reap that keeps me up at night. Most of the media and the broader discourse surrounding climate change portray it as a challenge that's problematic because we know what's going to happen. The deeper reality is that it is problematic because we often don't know what's going to happen.

The Earth's climate is an incredibly complex system. What keeps me up at night is how every time we try to abstract complex systems into single variables, be they temperature, carbon dioxide emissions, or some other factor, we run into problems. What we measure is what we manage and optimize for. Measuring, managing, and optimizing for single variables, be they gross domestic product, energy production, or wealth, is what always gets us into trouble.

I don't always see climate practitioners, including myself, fundamentally shifting from this in a paradigmatic-defining way. One more 2023 challenge that’s also an opportunity for 2024.

What gets me out of bed in the morning?

You. Truly! There is no way around the many challenges that climate change presents us with. There is only through. By pressing headlong into complexity, discomfort, and challenge. You, the readers of this newsletter, are the people ardently doing this work in all its forms and flavors.

Also, to weave together two topics we’ve already hit (resisting dualities and U.S. oil production), here’s something I wrote in March that still resonates and reverberates for me, writing this now:

I can tell myself two stories about the Willow Project's approval and hold them both true. I contain multitudes.

For one, at the most macro level, you'd be hard-pressed to find signs of progress on climate goals if you looked at global supply and demand for oil, coal, and natural gas. They're at all-time highs.

That's discouraging. It makes me, truthfully, lie on the floor of my apartment and wonder what we're accomplishing in climate tech.

On the flip side, if it weren't for clean energy, growth in new EV sales, or the other tech undercurrents we track in this newsletter, demand for fossil fuels and global emissions would be higher. Progress is often 'sub-surface' for a while before it becomes exponential enough to make an observable dent at a global scale. That's hope I hold onto.

On a personal note

The most important things I did this year included:

I was a great friend

I was a great brother & uncle

I was a good son

I worked on my master 'craft' every day

I was (pretty) good to my mind, body, & soul

I was open-minded & curious

Note that none of this is inherently dependent on a 'career' or relates to climate, per se. Still, these are the building blocks, at least in my experience, of all productive, thoughtful, duality-denying climate action and work.

And there is also a salient connection in one of those bullets to your reading this and my writing this. My master 'craft' is what I'm doing here right now. I've spent this year homing in on the one thing I can do for the rest of my life: Synthesizing and curating a lot of seemingly disparate information, data, conversations, and my own lived experience into words on a page. Getting clear on how and why that is my master craft has been the biggest win for me personally in 2023. What’s yours?

Thanks for being here for my journey. Hope all serves you. It serves me.

Wishing you all the best for the rest of the year

— Nick

Reply